Introduction

Many people have had to lean on the social security system during the pandemic, some for the first time — the number of people claiming Universal Credit increased by 98% between January 2020 to June 2021 to six million.[i]

Pandemic-era research[ii] has already found that many benefit claimants have experienced serious economic stress since the pandemic struck, despite the Government’s temporary £20 uplift for those claiming Universal Credit and Working Tax Credit.[iii] For example, recent Bright Blue analysis[iv] found that significant minorities of Universal Credit claimants reported not being up to date with household bills and housing payments throughout the pandemic,[v] with a significant minority also reporting finding it difficult to manage financially throughout the pandemic.

As part of Bright Blue’s ongoing project examining the inequalities of home working during the pandemic, we investigated differences in the experiences of benefit claimants and the rest of the public in the first year of the pandemic.

Our analysis uncovers two types of experience during the pandemic where significant differences between benefit claimants and the rest of the public emerge: financial and relational.

Methodology

Polling was undertaken by Opinium and conducted between 19th and 26th February 2021. It consists of one sample of 3,003 UK adults, with 1,053 respondents who are benefit claimants and 1,950 respondents who are not benefit claimants. Benefit claimants refers to those receiving at least one benefit, such as Universal Credit or Disability Allowance. The sample was weighted by Opinium to reflect a nationally representative audience.

Financial

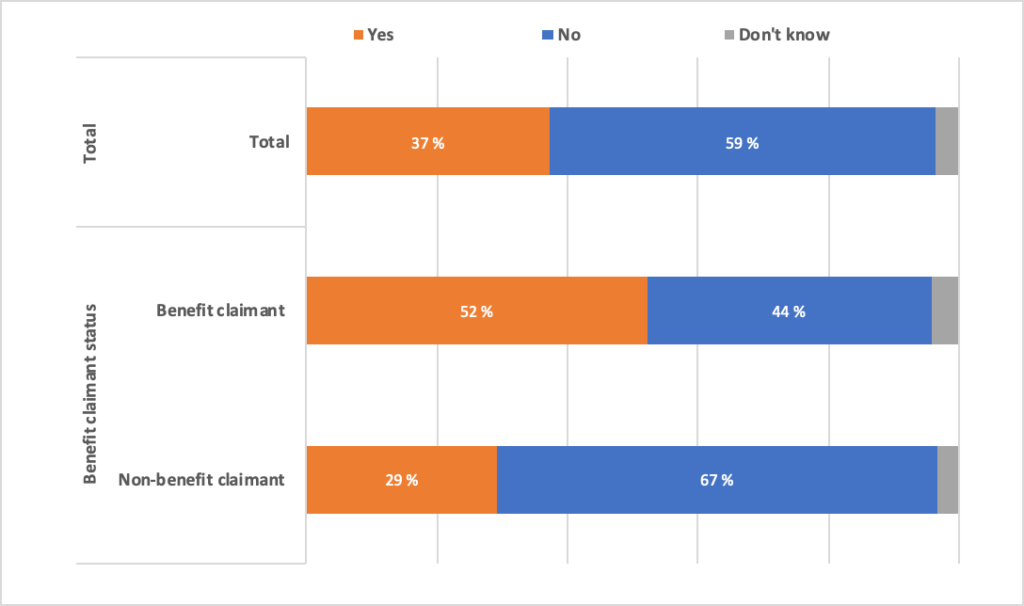

Benefit claimants are significantly more likely than the rest of the public to report having to dip into their savings to cover daily expenses over the first year of the pandemic, as can be seen in Chart 1 below.

Chart 1. Views of the UK public on whether they have had to dip into their savings to cover daily expenses or not since March 2020, by benefit claimant status.

Base: 3,003 UK adults

While a majority of 52% of benefit claimants report having to dip into their savings to cover daily expenses over the first year of the pandemic, a minority of 29% of the rest of the public report the same. Indeed, the majority of the rest of the public (67%) report not having to dip into their savings to cover daily expenses since March 2020.

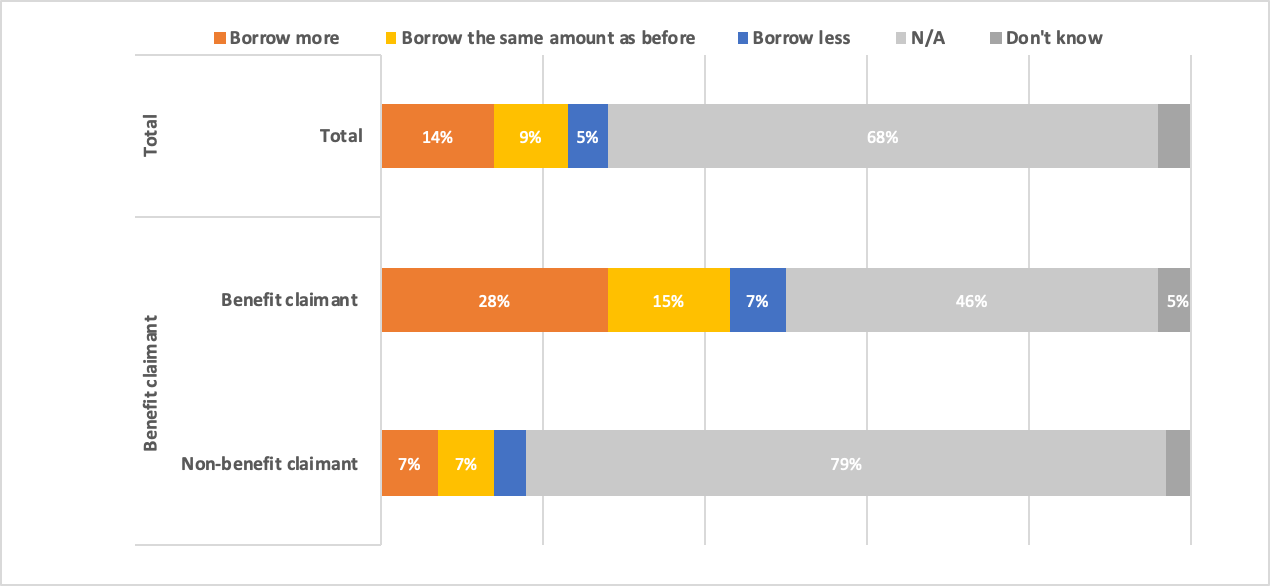

Benefit claimants are not only more likely than the rest of the public to report being forced to erode their savings in order to afford daily expenses over the course of the first year of the pandemic, but also to have to borrow more money to cover these daily expenses, as is demonstrated in Chart 2 below.

Chart 2. Views of the UK public on whether they are borrowing more, the same amount as before, or less money to cover daily expenses since March 2020, by benefit claimant status.

Base: 3,003 UK adults

Though a plurality of benefit claimants report that they did not have to borrow money to cover daily expenses before March 2020 and still did not after a year (46%), over a quarter do report having to borrow more money to cover daily expenses (28%) over the first year of the pandemic. Fifteen percent report borrowing the same amount of money as before and 7% report borrowing less.

In contrast, a firm majority of 79% of the rest of the public report that they did not did not have to borrow money to cover daily expenses before March 2020 and still do not, with only a small minority of 7% of them reporting that they have had to borrow more money during the first year of the pandemic. Seven percent of the rest of the public report borrowing the same amount of money as before and 4% report borrowing less.

In summary, benefit claimants appear to have been more significantly impacted by the pandemic financially than the wider public: they have been at a higher risk of being forced to lean on their savings and to borrow more money simply to be able to cover daily expenses over the first year of the pandemic.

Relational

Disturbingly, we also found a marked difference between benefit claimants and the rest of the public in terms of their likelihood of experiencing domestic abuse since the pandemic began. We focus on this as some evidence has emerged that lockdown measures have seen the incidence and intensity of domestic abuse increase.[vi]

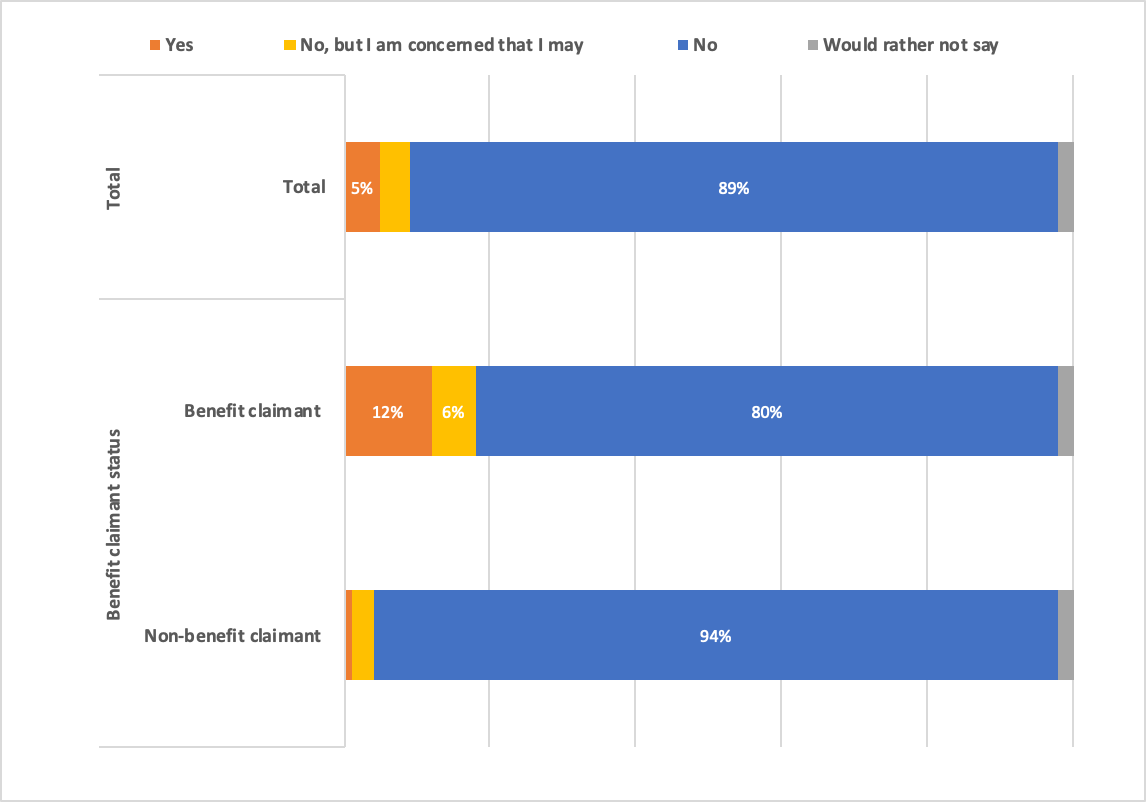

Asked whether, since March 2020, they have experienced domestic abuse, our polling shows that benefit claimants report experiencing domestic abuse during the first year of the pandemic at a much higher rate than the rest of the public, as is shown in Chart 3 below.

Chart 3. Views of UK adults on whether they have experienced domestic abuse since March 2020, by benefit claimant status.

Base: 3,003 UK adults

Though a clear majority (80%) of benefit claimants report that they have not experienced domestic abuse since March 2020, 12% of report that they have and 6% report that they have not but are concerned that they may.

In comparison, 94% of the rest of the public report that they have not experienced domestic abuse, 1% report that they have and 3% that they have not but are concerned that they may.

This means that there is a 14-percentage point difference between benefit claimants and the rest of the public in having experienced or been at serious risk of domestic abuse during the first year of the pandemic.

Previous research shows that those in lower income groups are at a higher risk of domestic abuse. Though benefit claimants are a diverse and broad group, the link between lower incomes and a higher risk of domestic abuse may in part explain what we have found: that benefit claimants have been at a disproportionate risk of domestic abuse during the pandemic in comparison with the rest of the public.

Conclusion

In providing insight into particular aspects of the financial and relational experiences of benefit claimants during the pandemic, our polling analysis puts a spotlight on how they have experienced the first year of the pandemic differently to the rest of the public.

We have found that not only have benefit claimants been at a higher risk of experiencing domestic abuse during the first year of the pandemic, but that the pandemic has acted to undermine their financial resilience.

Notes

The relevant data tables for the polling can be found here.

We are grateful to Opinium for advising on and carrying out the survey, and to Barrow Cadbury Trust and Trust for London whose sponsorship have made this work possible. Barrow Cadbury Trust and Trust for London do not necessarily endorse this analysis, over which Bright Blue retains complete editorial control.

References

[i] ONS, “Universal Credit statistics, 29 April 2013 to 10 June 2021”, https://www.gov.uk/government/statistics/universal-credit-statistics-29-april-2013-to-10-june-2021 (2021).[ii] Patrick Butler, “One in six new universal credit claimants forced to skip meals”, The Guardian, 19 February, 2021.

[iii] K. Summers et al., “Claimants’ experiences of the social security system during the first wave of COVID-19”, Welfare — At A Social Distance and Economic and Social Research Council (2021).

[iv] Anvar Sarygulov, “Benefit to all? Financial experience of Universal Credit claimants during the pandemic”, Bright Blue, http://www.brightblue.org.uk/benefit-to-all/ (2021).

[v] “New projects”, Bright Blue, http://www.brightblue.org.uk/research/.

[vi] Ryan Shorthouse and Phoebe Arslanagić-Wakefield, “Domestic abuse is everyone’s business”, ConservativeHome, https://www.conservativehome.com/platform/2021/02/ryan-shorthouse-and-phoebe-arslanagic-wakefield-domestic-abuse-is-everyones-business.html (2021); ONS, “Domestic abuse in England and Wales overview: November 2020”, https://www.ons.gov.uk/peoplepopulationandcommunity/crimeandjustice/bulletins/domesticabuseinenglandandwalesoverview/november2020 (2020).

[Image: Engin Akyurt]