Unnecessary age restrictions

I named the Lifetime ISA (LISA) as such because it was intended that it should serve from cradle to grave. The objective was to encourage saving early, and to harness the positive power of compounding over many years. The ISA range could then be rationalised; there are far too many different ISAs. Instead, the Treasury chose to restrict being able to open a LISA to those aged between 18 and 39, although account holders can then continue contributing into it until the age of 50.

These age-related rules add to complexity, are limiting and unnecessary, thereby dampening demand. They serve no consumer purpose.

The Treasury should consider the following two age-related enhancements to the LISA:

- From birth. Contributions should be permitted from birth rather than from 18 but, other than a £500 starter bonus (reminiscent of the last Labour Government’s Child Trust Funds), they should not attract 25% bonuses until 18.[5] Nor should access be permitted until 18. The Junior ISA would be immediately rendered redundant.

We could go further: a LISA could be automatically established when a baby’s name is registered, with a provider nominated by the parents, as the personal saving equivalent of workplace auto-enrolment.

The question of whether 25% bonuses should be paid on pre-18 contributions is for debate. Critics may argue that bonuses would disproportionately benefit wealthy families, but any form of means-testing would add unwarranted complexity.

- Until death. The age ceiling for contributions should be removed. Any contributions made from the age of 50 onwards should be locked in for at least ten years, to ensure a term commitment to saving in return for the bonuses. This would eliminate the risk of ‘round tripping’ either side of 60.[6] A similar restriction, in fact, should be placed on private pension contributions, which are accessible days after the receipt of tax relief – that is, either side of the 55th birthday.

The withdrawal penalty: eliminate it

LISA withdrawals made before the age of 60 may be used, without penalty, to buy the first home (costing no more than £450,000).[7] Consequently, the bonus is retained. However, pre-60 withdrawals used for other purposes incur a 25% early withdrawal charge. This is widely misunderstood, and a source of great confusion because it is more than the 25% bonus initially received. Consider an example:

- £100 is saved in a LISA, attracting a £25 bonus, for a total of £125.

- Subsequently the £125 is withdrawn, but not before deduction of a 25% charge. £125 x 25% = £31.25p.

- Consequently, the saver ends up with £93.75p in his pocket, having initially contributed £100. Thus, the withdrawal has cost him both his initial bonus and an additional £6.25 (6.25% on the initial amount saved).

This charge (mischievously misrepresented as a 25% ‘penalty’) is actually a 6.25% ‘penalty’, after return of the bonus. It sabotages the frictionless reversibility inherent in my original proposals. Penalty-free access to savings will encourage people to start saving, comforted by the knowledge that a change of mind (to spend rather than save) will not incur a penalty. Inertia could then be allowed to do its work. Note that conventional Stocks and Shares ISA savings are sticky, notwithstanding the ready access to them. Indeed, an increasing number of people consider ISAs as part of their retirement savings (imitating Australia’s pensions tax regime, which is much nearer to TEE (‘Taxed’, ‘Exempt’, ‘Exempt’).[8]

Notwithstanding the 6.25% early withdrawal penalty, the Lifetime ISA is a far cheaper source of cash than many forms of consumer borrowing: for many people, the penalty is not a meaningful deterrent to early access. In addition, it is not intuitive: it risks confusion, adds to complexity and, crucially, it serves no consumer purpose. Furthermore, the penalty undermines a fundamental objective that I set for the LISA: fluid reversibility, cost-neutral for both parties (saver and the Treasury).

The Office of Tax Simplification (OTS) has acknowledged the withdrawal penalty’s scope to confuse, noting that it adds to the challenge on giving advice.[9] It concluded that the Government should revisit the rules on early withdrawals from the LISA, not least to ensure that the LISA rules work effectively for unadvised retail savers.

The Treasury could eliminate the penalty by reducing the early withdrawal charge to 20%, for example.:

- £100 is saved a LISA and attracts a £25 bonus, for a total of £125.

- Subsequently the £125 is withdrawn, but not before deduction of a 20% charge. £125 x 20% = £25.

- Consequently, the saver ends up with £100 back in his pocket: cost neutrality for both parties (saver and Treasury).[10]

The 20% charge could be presented as: ‘If you change your mind, and want access to your savings before reaching later life, you simply repay the bonus you initially received’.

An opportunity to reinforce automatic enrolment (AE)

Automatic enrolment (AE) into workplace pension schemes has now entered its ramp up’ phase in respect of statutory minimum contribution rates. Employee contributions are in the process of quintupling, from 0.8% of band earnings to 4.0% by April 2019, potentially against a backdrop of rising mortgage rates and stagnant real earnings growth. We should expect opt-out rates to rise.

This risk could be reduced by increasing the sense of personal ownership of savings derived from the workplace. All savings should be as personal as a bank account, ideally without all the jargon and paraphernalia of pension pots. And being in control is closely allied to being motived, and therefore engaged, which would likely discourage AE opt outs. Indeed, it could encourage larger contributions.

The LISA should be included within AE legislation’s definition of a qualifying’ scheme, eligible to receive (post-tax) employee contributions, attracting the 25% bonus. This would provide improved access to their own contributions (relative to pension pots), and would particularly appeal to younger generations, especially ‘Generation Y’,[11] many of whom are prioritising saving for a home over saving for retirement. And employees would not miss out on AE’s employer contributions.

A LISA within the AE framework should be afforded the same consumer protections as occupational pension pots, including a charge cap, and perhaps a low-cost default fund. Consideration should also be given to a trustee-based governance structure, and including the LISA within the remit of The Pensions Regulator (TPR).

A previous paper I authored for the Centre for Policy Studies describes in detail how the LISA could be accommodated within the AE framework.[12]

The self-employed

The LISA is well-suited to those with no access to an employer-sponsored scheme, including the self-employed, who are ineligible for AE. Fewer than one in three (31%) of freelance workers (notably the self-employed) are currently paying into any pension at all: this must be addressed.[13] Their Class 4 NICs rate, at 9%, is 3% less than employees’ Class 1 NICs, yet the self-employed accumulate the same State Pension entitlement. This is unreasonable.

Class 4 NICs could be increased by 3% but characterised as bonus-eligible ‘auto-contributions’ to a Lifetime ISA. These should be accompanied by a default which would redirect the 3% to HMRC, triggered by non-payment of a bonus-eligible ‘quasi-employer’ contribution, which could, to some degree, count as a tax-deductible business expense. Both auto-contributions and quasi-employer contributions could be ramped up in the style of AE, increasing in 1% annual increments, to 3% each by 2021, say.

An opportunity to simplify the ISA range

Today there are six different ISAs: Cash ISA, Stocks and Shares ISA, Junior ISA, Help to Buy ISA, Innovative Finance ISA, and the Lifetime ISA.

If the LISA’s age restrictions were removed then the Junior ISA would be instantly redundant. In addition, with the withdrawal penalty scrapped to facilitate cost-neutral reversibility, we would not need the Cash ISA (the tax rationale for it is already undermined by the Personal Savings Allowance) or the Stocks and Shares ISA, because the LISA could hold both cash and securities. Furthermore, lack of demand would justify scrapping the Innovative Finance ISA. The Help to Buy ISA is already set to close (30 November 2019), superseded by the LISA (which has a more generous incentive).

This would leave us with one ISA, the Lifetime ISA, to serve from cradle to grave. Ideally there would be no limit on the amount that could be contributed but there would, of course, have to be an annual bonus cap (determined by Treasury affordability, discussed in my recent Centre for Policy Studies paper[14]).

Taxation

The Lifetime ISA trumps saving in a personal pension pot (such as a SIPP) in two fundamental respects: tax treatment and access flexibility.

Tax nomenclature

As mentioned earlier, savings products are codified chronologically for tax purposes. Pensions are ‘EET’ – that is, ‘Exempt’ (contributions attract tax relief), ‘Exempt’ (income and capital gains are untaxed), and ‘Taxed’ (capital withdrawals are taxed at the saver’s marginal rate). Conversely, as discussed earlier, ISA contributions are made from post-tax income, but withdrawals are tax free. Hence ISAs are ‘TEE’.

The up-front incentive

The LISA’s upfront incentive is very deliberately detached from tax-paying status. This overcomes the regressive problem, whereby the wealthy receive most of the tax relief. The result is the 25% bonus. As Bob Scott, Chairman of the Association of Consulting Actuaries, said: “Surveys had shown public support and enthusiasm for ISA-style products, particularly if there was some tangible bonus or ‘sweetener’ from the government”.[15]

Consider a basic rate taxpayer who earns £100 gross, £80 net. She could either:

- contribute £80 into a LISA. The Treasury then adds a 25% bonus, £80 x 25% = £20, for a total of £100; or

- contribute £80 into a SIPP, say, to which tax relief of £20 is automatically added by the provider, for a total of £100 in the pot.

For basic rate taxpayers (92% of the under-40s workforce[16]), the LISA’s 25% bonus and pension pots’ 20% tax relief are economically equivalent. Many people do not appreciate this. The confusion arises because the LISA’s 25% bonus is determined using contributions made from post-tax income, whereas pensions’ tax relief is expressed as a percentage of gross (pre-tax) income.

There is a small minority for whom a personal pension product makes more economic sense than a LISA, notably high earners with access to higher (40%) or additional (45%) rates of tax relief (see Table 1 below).

Drawdown

Drawings from pension pots, currently permitted from the age of 55, are taxable at the marginal rate, whereas, from 60, LISA drawings are tax-free, accumulated 25% bonuses being retained.

The financial impact of different tax treatments

The LISA is ostensibly a TEE product, yet for basic rate taxpayers (working or retired) it is effectively entirely tax-free, akin to EEE. The 25% bonus, being economically equivalent to 20% Income Tax, effectively neutralises basic rate Income Tax paid before contributing to a LISA. The front ‘T’ is, in practice, an ‘E’ for basic rate taxpayers.

Remarkably few people appreciate this fundamental LISA attribute, one with which the private pensions framework cannot compete. The latter’s effective tax rate is 15% for basic rate taxpayers, after taking the 25% tax-free lump sum into account.

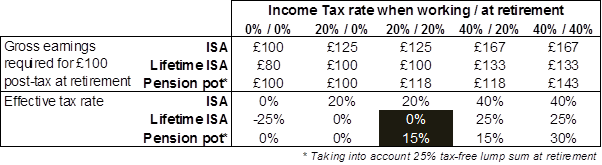

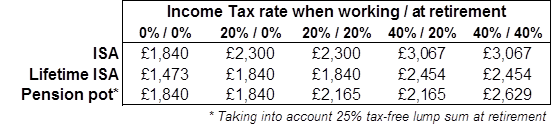

Table 1 below compares the gross (pre-tax) earnings required to produce a post-tax £100 in retirement (drawdown), for ISAs and pension pots assuming no interim capital growth. It also shows the effective rate of Income Tax.

Table 1. ISAs, LISAs and pension pots compared

Table 1 shows that for the most common tax combination (20% while working and in retirement) the LISA has an effective tax rate of 0%, whereas it is 15% for pension pots. The LISA is particularly attractive to non-taxpayers (low earners) because they benefit from a negative tax rate via the 25% bonus. Conversely, a pensions product is a better choice for workers paying 40% Income Tax because their tax relief exceeds the LISA bonus of 25%. But fewer than 8% of the under-40’s pay more than the basic rate of Income Tax.[17]

In reality, the LISA’s tax advantage over pension products is likely to prove more significant than Table 1 suggests. Consider someone saving over a 30-year period in a 2% real investment growth environment, with contributions also increasing at 2% per annum. Table 2 shows the initial annual contribution required to accumulate £100,000 post-tax after 30 years.

Table 2. Initial annual contribution to accumulate £100,000 post-tax after 30 years, assuming contributions and assets grow at 2% per annum

Table 2 shows a similar pattern of results as Table 1, with basic rate taxpayers having to contribute 18% more to a pensions pot than a Lifetime ISA for the same post-tax £100,000 at retirement. The LISA’s tax advantage over a pensions pot is accentuated because, unlike pensions pots, 30 years’ of capital growth and accumulated income within a LISA is not taxed in drawdown.

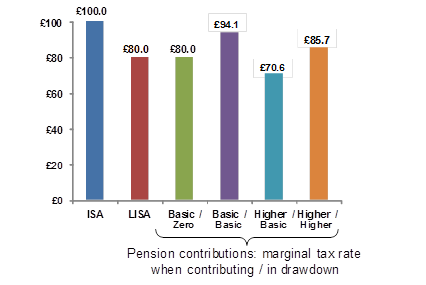

Another way of comparing saving in a LISA with saving in a pensions product is to look at the post-tax contribution required to generate a post-tax £100 in retirement, as shown in Figure 1 below.

Figure 1. Post-tax contribution for a post-tax £100 in retirement

For example, a basic rate taxpayer who subsequently paid basic rate tax in retirement would have to contribute a post-tax £80 to a LISA, but £94.1 to a pension pot, to receive a post-tax £100 in retirement.[18] The LISA is more tax-efficient, but there is also its early-access optionality to consider.

Access

There are almost no circumstances in which pension pot assets can be accessed before the age of 55 (57 from 2028, still out of kilter with improvements in life expectancy; it should be swiftly raised to 60).[19] LISA assets, however, may be readily accessed, either by paying the early withdrawal penalty or, in respect of purchasing the first home, without penalty.[20] Unconditional penalty-free LISA access commences at 60, five years later than pension pot access, but this is likely to be immaterial to younger generations, specifically Generation Y, when deciding, today, between the two saving products.

For younger generations who prioritise home ownership over saving for retirement, the LISA’s ready access when buying the first home, with accumulated bonuses retained, is a valuable free option. Generation Y in particular are now discovering that pension pots cannot compete with this.

As an aside, the LISA has a £450,000 cap on the cost of a first home purchase: it is unclear what behaviour this is trying to encourage (or discourage), or what consumer purpose it serves. The cap just adds to product complexity: it should be scrapped.

Other differences between LISA and a pensions product

There are several other differences between the LISA and a pensions product. They appear to be arbitrary features on the savings landscape, only adding to its complexity. All are immaterial to younger generations, with no evidence that they influence behaviour in respect of deciding between saving in a pension pot or a LISA. They serve no meaningful consumer purpose.

The annual contribution limit

Annual contributions to the Lifetime ISA are capped at £4,000, which places an annual £1,000 ceiling on the bonus. Contributions sit within the overall ISA annual limit of £20,000 (from April 2017), up over 31% on 2016 (and a clear indication of the direction of travel for savings policy). There is no limit to what may be contributed to pensions pots, although the annual allowance restricts tax relief to the first £40,000 of contributions, which is irrelevant to over 99% of the population.

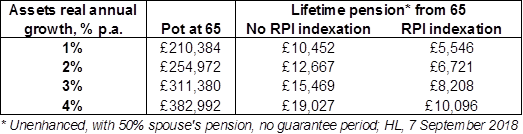

At first sight, the LISA’s £4,000 looks modest, but not once the combination of starting early and the positive power of compounding are taken into account. If the contributions upper age limit were removed, and recognising that few 18 year olds will be saving £4,000 per year, Table 3 illustrates the LISA asset size after 35 years of contributions and bonuses (regular saving from the age of 30). It also shows the lifetime annuity (‘pension’) that could be secured at 65.

Table 3. LISA pot size and lifetime annuity after 35 years of contributions

Assuming a 2% annual real growth rate for investments (net of costs), the LISA would have accumulated assets of over £254,000 at the age of 65.[21] This would be sufficient to generate a lifetime RPI-indexed pension of over £6,700 from the age of 65 (or over £12,600 without RPI indexation), with 50% spouse’s pension.

There is, however, a second perspective to consider in respect of the LISA’s contributions limit. Given that first-time buyers need an average deposit of nearly £33,000 (over £106,000 in London, where the average house price paid by first-time buyers was £409,795), some 16% (26%) of the purchase price, the £4,000 annual limit could be considered as low.[22] Meanwhile, the LISA is unlikely to have much impact on house prices, certainly in the short to medium term.

Inheritance Tax (IHT)

Pension pots are sheltered from IHT, whereas ISAs are not. But how many people in their twenties and thirties are worrying about paying IHT, as opposed to having access to savings to buy their first home, say? Pension pots’ IHT advantage is a red herring in terms of influencing the savings behaviour of younger generations.

In later life, however, IHT is a significant consideration for some people, which influences the order in which assets are drawn down (the ‘batting order’). The current arrangement encourages pension assets to be left until last. It is ludicrous that they are exempt from IHT simply because they reside within a pensions wrapper, not least because contributions are likely to have received up-front tax relief. In addition, unutilised capital growth and income are untaxed. Post-death, pension assets should be taxed as per other savings, in the interests of fairness (to future generations), and as a simplification.

Means-tested benefits

Pension assets are excluded from means-testing assessments in respect of state benefits, whereas LISA assets are not. But access to benefits is highly unlikely to be a consideration when choosing a savings vehicle.

Adviser charging

Unlike pension pots (and other ISAs), the LISA rules make no provisions for adviser charging (the practice of withdrawing money from a tax wrapper to pay for advice). Consequently, using LISA funds (pre-60) to pay for advice incurs the penalty charge: changing this rule would most likely encourage more LISA uptake through advice channels.

Conclusion

The LISA has the potential to help catalyse a much more broad-based savings culture, but it is unnecessarily complex. Simplification, and a role for it within automatic enrolment, could nudge financial industry to engage with it more assertively. It could then be rewarded with a much broader customer base.

This paper makes three main proposals to achieve this:

- Liberate the LISA of its age restrictions

Contributions should be permitted from birth rather than from age 18 but, other than a £500 starter bonus, they should not attract the 25% bonuses until 18, and no access should be permitted until 18. We could go further: a LISA could be automatically established when a baby’s name is registered, with a provider nominated by the parents, as the personal saving equivalent of workplace auto-enrolment.

In addition, the contributions age ceiling should be removed, with the caveat that any contributions made from age 50 onwards should be locked in for at least ten years (with allied bonuses). This would ensure a term commitment to saving in return for bonuses.

- Introduce penalty-free access

-

The 25% charge imposed on pre-60 withdrawals is widely misunderstood because it is not the same as the 25% bonus initially received.

[23]

-

There is an implicit 6.25% ‘penalty’ which is not intuitive, it adds complexity and serves no consumer purpose.

[24]

It should be eliminated, by simply reducing the withdrawal charge from 25% to 20%. Penalty-free access to savings would encourage more people to save more, and would be cost neutral to the Treasury.

- Include the LISA to bolster AE

Employee contributions made under AE should be eligible for payment into a LISA, attracting the 25% bonus. This would help engender a sense of personal ownership of savings derived from the workplace, as well as provide improved access (to buy the first home): the risk of rising AE opt-out rates should then diminish. All savings should be as personal as a bank account.

If these three proposals were implemented, then there would be no need for any other ISAs. The Lifetime ISA could serve as a single savings vehicle from cradle to grave.

The LISA’s 25% bonus, determined using contributions made from net (post-tax) income, is equivalent to 20% Income Tax relief (which is expressed as a percentage of gross (pre-tax) income). Consequently, for basic rate taxpayers, LISA savings are effectively entirely tax-free if kept until 60. Remarkably few people appreciate this fundamental LISA attribute. Conversely, the effective tax rate of pension pot assets is 15% for basic rate taxpayers.

In addition, the LISA contains a valuable free option; ready access when buying the first home, with accumulated bonuses then retained. Generation Y is slowly discovering that pension pots cannot compete with this. There have been many surveys of attitudes towards the LISA: it is clear that younger generations like it.

Michael Johnson is an Associate Fellow at Bright Blue and a Research Fellow at the Centre for Policy Studies.

Michael trained with JP Morgan in New York and, after 21 years in investment banking, joined Towers Watson, the actuarial consultants. Subsequently he was responsible for the running of David Cameron’s Economic Competitiveness Policy Group.

Michael is the author of more than 40 pensions-related papers published through the CPS, sometimes supported by both Conservative and Labour peers. A number of his proposals have been implemented, including the scrapping the annuitisation requirement (“freedom and choice”), the pooling of the LGPS’s funds, and the introduction of the Lifetime ISA and bonus. More recently he detailed proposals for a Workplace ISA to compete with occupational pension products, residing within the Lifetime ISA.

In April 2018 the Work and Pensions Select Committee endorsed three of Michael’s earlier proposals: there should be a new default decumulation pathway to support the disengaged (“auto-protection”); that NEST should be permitted to provide it; and there should be a single, public, mandatory pension dashboard.

Michael is occasionally consulted on pension reform by serving Ministers, shadow Ministers and the Cabinet Office. He has given oral and written evidence to Select Committees in both Houses of Parliament.

The views expressed in this essay are those of the author, not necessarily those of Bright Blue.

[1] Centre for Policy Studies, Introducing the Lifetime ISA, August 2014.

[2] Lifetime Isa providers: AJ Bell; Foresters Friendly Society; Hargreaves Lansdown (48,000 accounts, June 2018); Moneybox; MetFriendly (police only); Nottingham Building Society (cash only); Nutmeg (11,000 accounts); One Family; Scottish Friendly; Skipton Building Society (cash only; 110,000 accounts); The Share Centre; and the Transact platform.

[3] HMRC, “Table 9.4, Individual Savings Account (ISA) Statistics”, August 2018.

[4] House of Commons’ Treasury Select Committee, Household finances: income, saving and debt, 18 July 2018.

[5] Child Trust Funds’ initial payment was up to £500, dependent on household income; they were scrapped in January 2011.

[6] ‘Round tripping’: whereby LISA savings on which a bonus has been paid are withdrawn and then re-contributed into the LISA to attract another bonus.

[7] In addition, no penalty is incurred when transferring to a different Lifetime ISA provider, or in respect of withdrawals by someone who is terminally ill and expected to die within 12 months.

[8] Savings products are codified chronologically for tax purposes. ISA contributions are made from post-tax income, but withdrawals are tax-free. Hence the coding ‘TEE”’.

[9] Savings income: routes to simplification; Office of Tax Simplification, HM Treasury, May 2018.

[10] Bar the Treasury’s economic interest in a LISA’s interim asset performance. If assets increase, the 20% penalty would be larger in cash terms than the original 25% bonus, and vice-versa

[11] Generation Y are ‘millennials’: (approximately) those born between 1980 and 2000 (aged from 18 to 38 today).

[12] Reinforcing auto-enrolment; a response to the DWP’s consultation; Michael Johnson, CPS, 2017.

[13] Based on research by IPSE, a trade body for the self-employed (May 2018).

[14] Michael Johnson, Five proposals to simplify saving, CPS, August 2018.

[15] Bob Scott, Chairman of the Association of Consulting Actuaries, speaking at the ACA’s annual dinner, 1 December 2016.

[16] Derived from HMRC and ONS tables.

[17] Derived from HMRC and ONS tables.

[18] A post-tax £94.1 contributed to a pension pot would receive £23.52 in tax relief, so £117.62 goes into the pot. At retirement 25% of this can be withdrawn tax-free (£29.4), leaving £88.22 to be taxed at 20%. This leaves £70.6 post-tax, plus the £29.4 = £100 post-tax.

[19] Exceptions include serious ill-health and those with a ‘protected pension age’ relating to a pension scheme joined before 6 April 2006.

[20] In addition, no penalty is applied in event of terminal illness (with less than 12 months to live) or when transferring to another Lifetime ISA with a different provider.

[21] Why ‘only’ 2%? We should be mindful of the risk of long-term flat or negative real returns from fixed income, sclerotic investment returns elsewhere, and a developed world potentially on the cusp of going ex-growth. Better to be cautious.

[22] Halifax First-Time Buyer Review, covering the first six months of 2017.

[23] 100 saved attracts a £25 bonus to equal £125. On withdrawal, £125 x 25% = £31.25p, i.e. £6.25p more than the bonus received on the £100 saved.

[24] There is no charge in respect of purchasing the first home.