Introduction

It has been much commented that young adults aged 18-34 have received a particularly raw deal over the past year: much less likely than older age groups to suffer the more serious health consequences of Covid-19, but much more likely to be disproportionately impacted in terms of their finances and freedoms thanks to pandemic lockdown measures.

As part of Bright Blue’s ongoing project examining the inequalities of home working during the pandemic, we wanted to ascertain whether there were differences by age in experiences, to explore whether young adults were indeed struggling more as a result of Covid-19 and the resulting lockdown measures.

Our analysis finds that there are three types of experience during the pandemic where significant differences between different age groups emerge: financial, psychological and relational.

Methodology

Polling was undertaken by Opinium and conducted between 19th and 26th February 2021. It consists of one sample of 3,003 UK adults, with 836 respondents aged 18-34, 997 aged 35-54 and 1,171 aged over 55. The sample was weighted by Opinium to reflect a nationally representative audience.

Financial

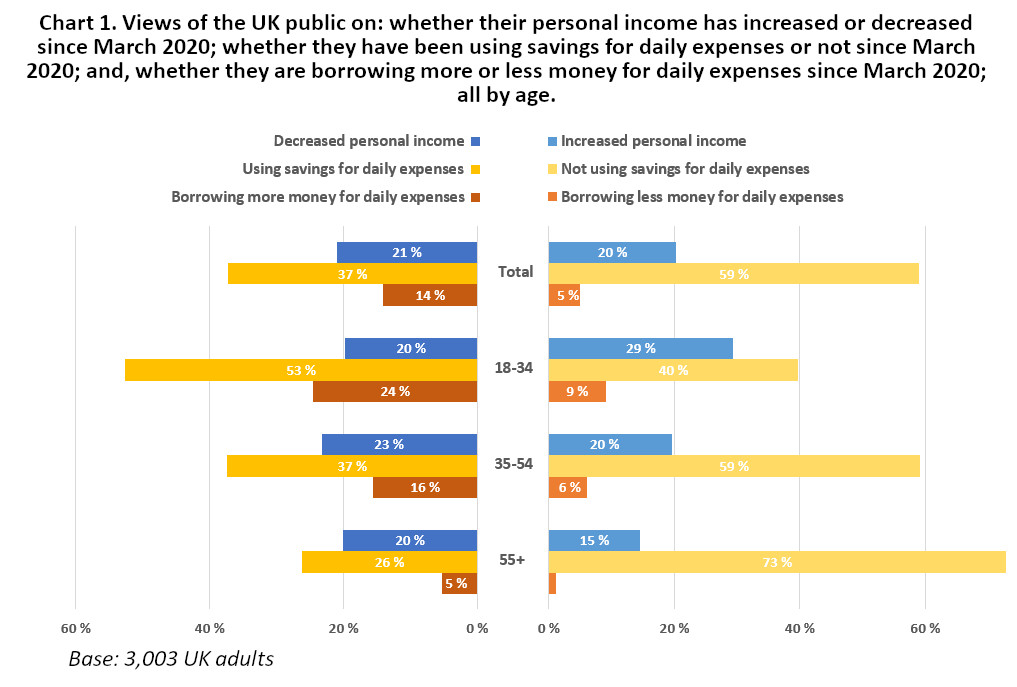

Those aged 18-34 are most likely to report their personal income has neither increased nor decreased since March 2020 (42%). But 29% of them report an increase and 20% report a decrease, meaning – somewhat surprisingly – that those aged 18-34 are the age group most likely to report that their personal income has increased since March 2020, as shown in Chart 1 below.

In comparison, 20% of those aged 35-54 and 15% of these aged over 55 report that their personal income has increased since March 2020. This means that 18-34 year olds are the only age group which are more likely to report they have experienced an increase in their personal income than a decrease since March 2020. This contradicts the prevailing assumption that young adults have fared worse financially as a result of Covid-19 and the resulting lockdown measures.

However, other data from Chart 1 paints a different picture. A majority (53%) of those aged 18-34 report having to dip into their savings to cover daily expenses since March 2020, while 40% report not having to do so, making those aged 18-34 the age group most likely to do so. In contrast, a minority of those aged 35-54 (37%) and over 55 (26%) report having to dip into their savings to cover daily expenses since March 2020, with a majority in both of these age groups reporting not having to do so (59% and 73% respectively).

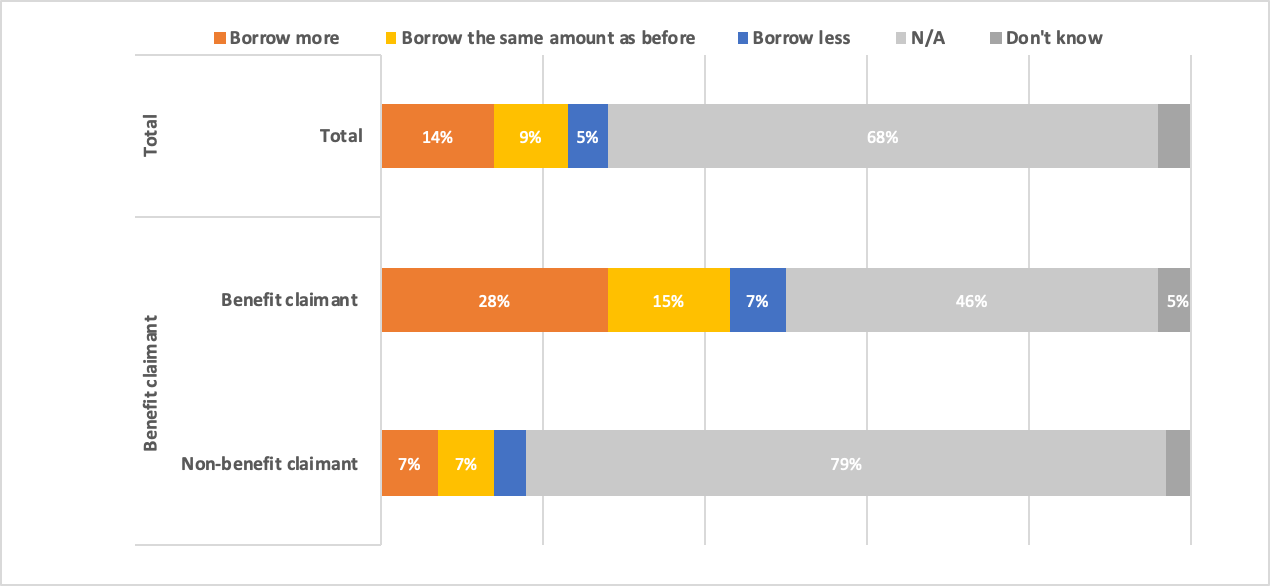

Young adults not only seem to have been more reliant on savings during the pandemic, but on borrowing too. Though those aged 18-34 were most likely to report that they did not have to borrow money to cover daily expenses before March 2020 and still do not (44%), nearly a quarter (24%) report having to borrow more money to cover daily expenses, making them the age group most likely to do so. Meanwhile, 14% reported borrowing the same amount as before and 9% borrowing less.

A majority of those aged 35-54 (62%) and aged over 55 (89%) report that they did not have to borrow money to cover daily expenses before March 2020 and still do not. Most notably, only 16% of these aged 35-54 and 5% of those aged over 55 report borrowing more to cover daily expenses.

Overall, young adults aged 18-34 in some respects have been financially worse impacted as a result of the pandemic and resulting lockdowns, relying on their savings and borrowing more. But in other respects – specifically whether their personal income has increased – young adults aged 18-34 are more likely to have done better than other age groups since March 2020.

Psychological

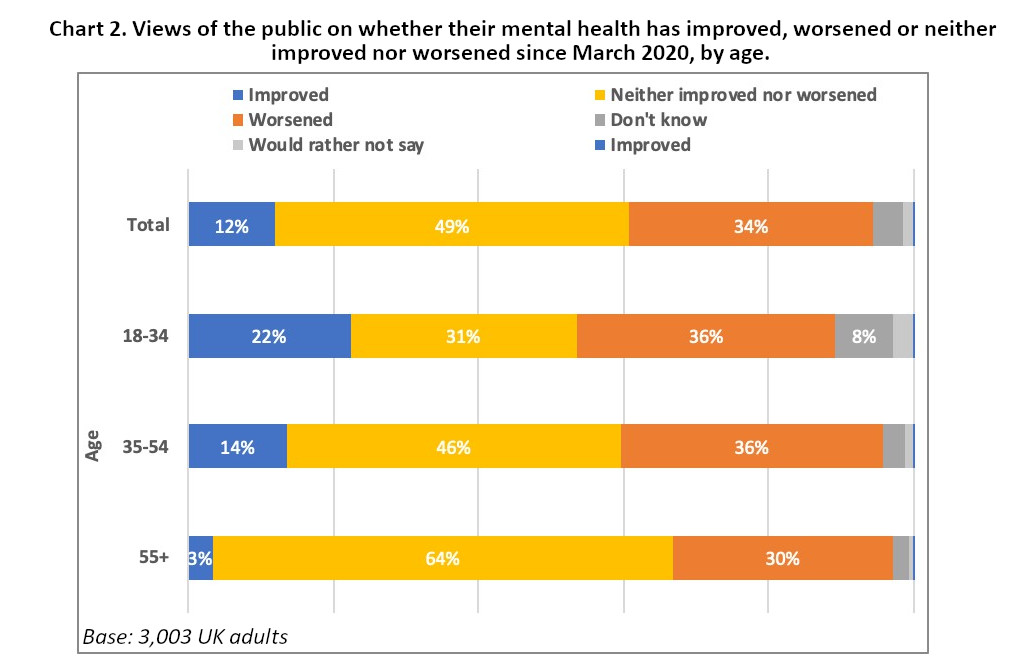

Having shown variation in financial experiences since the start of the pandemic relative to other age groups, we also found a differing impact of Covid-19 and lockdown measures on young people’s mental health. As Chart 2 below illustrates, asked whether, since March 2020, their mental health has improved, young adults are most likely to report it has worsened (36%). This means that those aged 18-34 are the only age group where the highest proportion of people report experiencing worsening mental health. However, interestingly, they are also the age group with the highest proportion of people reporting their mental health has actually improved, with over one in five (22%) of young people reporting this.

Meanwhile, those aged 35-54 are most likely report that their mental health has neither improved nor worsened since March 2020, with nearly half (46%) reporting this. However, the same proportion of 35-54 year olds report that their mental health has worsened as 18-34 year olds, with 36% reporting this. Meanwhile, a firm majority of 64% of those aged over 55 report that their mental health has neither improved nor worsened since March 2020, with 30% reporting it has worsened.

Yet, a much smaller proportion of those aged 35-54 (14%) and aged 55+ (3%) report that their mental health has improved during the pandemic relative to the youngest adults.

As such, when it comes to psychological experiences, young adults seem to have been the age group most likely to have experienced both better and worse mental health during the pandemic and resulting lockdown measures.

Relational

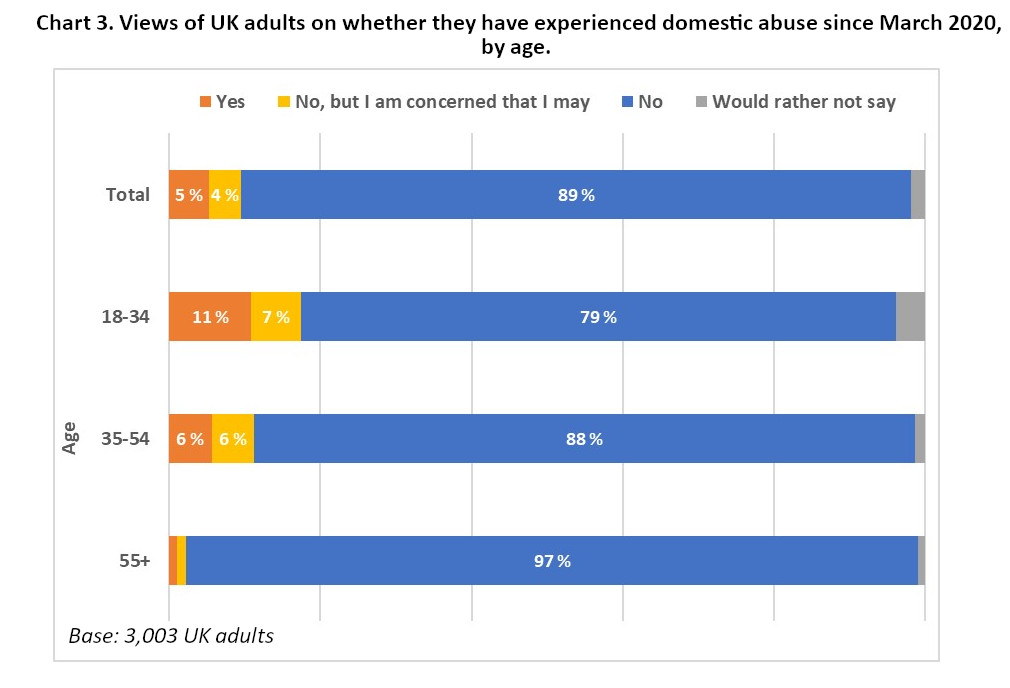

We also unearthed important differences by age group on a particularly sensitive subject: the experience of domestic abuse since the start of the pandemic. There are already widespread fears that this dreadful aspect of people’s relational experiences has grown in prevalence and intensity because of lockdown measures. [i]

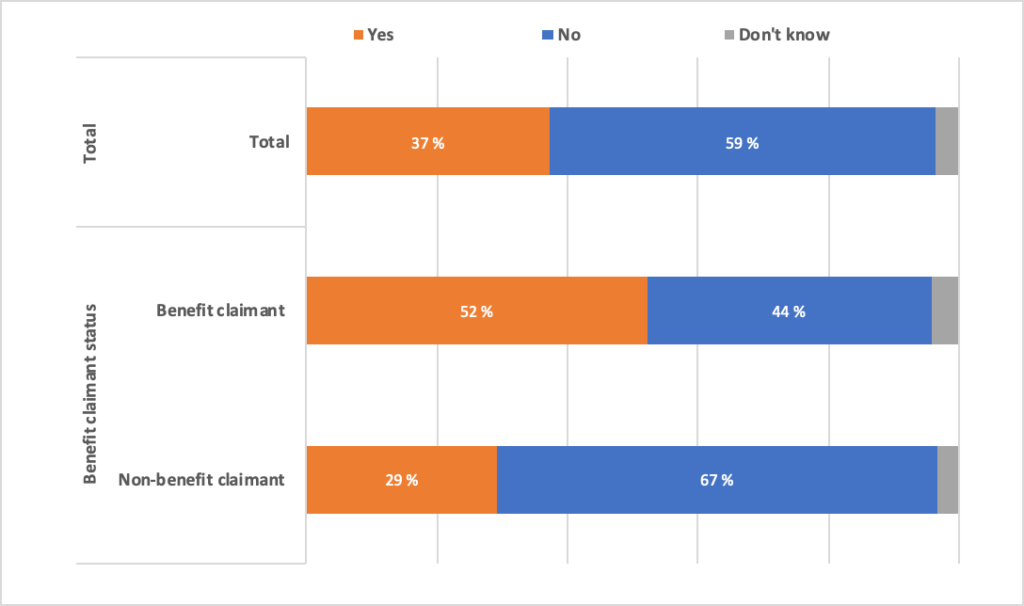

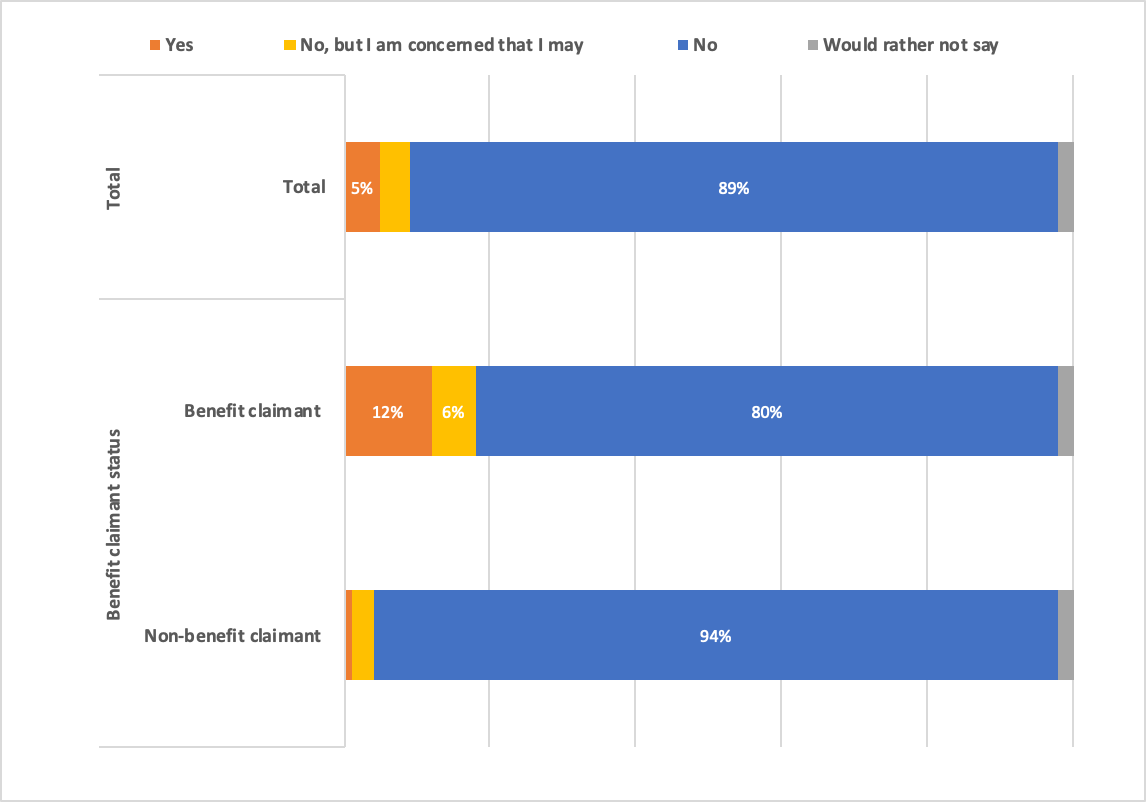

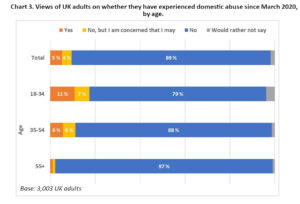

Asked whether, since March 2020, they have experienced domestic abuse, our polling shows that those aged 18-34 report experiencing domestic abuse since March 2020 at a higher rate than other age groups, as is shown in Chart 3 below.

Seventy-nine percent of those aged 18-34 report they have not experienced domestic abuse since March 2020. However, a troubling 11% report that they have and a further 7% that they have not but are concerned that they may.

In comparison, stronger majorities of those aged 35-54 (88%) and over 55 (97%) report they have not experienced domestic abuse since March 2020. Equally, smaller minorities of those aged 35-54 (6%) and over 55 (1%) report that they have experienced domestic abuse or that they have not but are concerned that they may (6% and 1% respectively).

Previous research has indicated that younger adults are at a higher risk of domestic abuse [ii], but our polling shows starkly that for nearly a fifth of young adults (18%), the homes we have all been forced to retreat to over the past year have not been a safe place.

Conclusion

Our polling provides a snapshot of particular aspects of the financial, psychological and relational experiences of those aged 18-34 during the pandemic.

Our analysis shows that the experience of those aged 18-34 since March 2020 is distinct in these experiences from that of older age groups. This age group are at a higher risk of having experienced domestic abuse since March 2020, while their experience around their finances and mental health has been much more mixed. Young adults seem to have been more likely to experience both better and worse financial and mental health during the pandemic and resulting lockdowns.

Notes

The relevant data tables for the polling can be found here.

We are grateful to Opinium for advising on and carrying out the survey, and to Barrow Cadbury Trust and Trust for London whose sponsorship have made this work possible. Barrow Cadbury Trust and Trust for London do not necessarily endorse this analysis, over which Bright Blue retains complete editorial control.

[i] Ryan Shorthouse and Phoebe Arslanagić-Wakefield, “Domestic abuse is everyone’s business”, Conservative Home, https://www.conservativehome.com/platform/2021/02/ryan-shorthouse-and-phoebe-arslanagic-wakefield-domestic-abuse-is-everyones-business.html (2021).

[ii] “Who are the victims of domestic abuse?”, Safe Lives, https://safelives.org.uk/policy-evidence/about-domestic-abuse/who-are-victims-domestic-abuse (2015).