Introduction

As the COVID-19 pandemic hit the UK in March 2020, the Government made an unprecedented intervention to support the incomes of households through increases in various working-age benefits and provision of job retention income support.

A major component of this was the ‘uplift’ to Universal Credit (UC) and Tax Credits, with most existing and all new working-age benefit claimants seeing a weekly £20 increase in their benefit payments. The provision of this uplift was extended several times over the last year or so as the pandemic continued, but it is now expected that the uplift will be withdrawn fully at the end of September 2021.

Evidence suggests that the COVID-19 pandemic has had a much greater negative economic impact on lower income households: they were more likely to face reductions in income, more likely to have to dip into savings[i], and more likely to accumulate debt.[ii]

This analysis focuses in particular on the financial impact of the pandemic on existing and new UC claimants relative to the rest of the public. We examine several objective measurements of financial security such as debt levels and households bills, as well as more subjective measures.

Methodology

Bright Blue has used survey data from the Understanding Society COVID-19 Study[iii] to perform original analysis examining changes in the actual and perceived financial situation of existing and new UC claimants relative to the rest of the population during the first year of the pandemic.

The Understanding Society COVID-19 Study conducts surveys at specific intervals, with questions varying between different survey waves. The months during the pandemic used in the analysis (May 2020, July 2020, November 2020 and March 2021) were chosen on the basis of availability of data on answers to financial questions.

Where possible, we have also included a comparison with responses to questions before Covid-19 hit, from the 2018-19 UK Household Longitudinal Study[iv], to illustrate the extent of change in the perceived and actual financial situation during the pandemic. However, as will be clear later in this analysis, two questions – on debt levels and on future perceptions of finances – did not have an appropriately similar question in 2018-19 for comparison purposes.

All survey data has been weighted to be representative of the adult population of the United Kingdom.

We examine three population groups: those who do not claim Universal Credit (‘non-UC’), those who were claiming Universal Credit in February 2020 (‘existing UC’), and those who began to claim Universal Credit in March 2020 or later (‘new UC’). While the non-UC group could include some claimants of other working-aged benefits, this group does provide a benchmark for how the broad population has been affected by the pandemic in terms of their perceived and actual financial situation. Unweighted sample sizes for each group and each time period are shown in Table 1 below.

Table 1. Unweighted sample sizes of each group of interest

| Time |

Non-UC |

Existing UC |

New UC |

| 2018-19 |

33561 |

757 |

N/A |

| May-20 |

14262 |

282 |

267 |

| Jul-20 |

12635 |

284 |

253 |

| Nov-20 |

11328 |

237 |

257 |

| Mar-21 |

11806 |

252 |

351 |

Source: University of Essex, Institute for Social and Economic Research. Understanding Society: COVID-19 Study, (2021) and University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 10, 2018-2020, (2020).

The difference between existing and new UC claimants is of interest because there is previous research that indicates that new UC claimants, who were forced to claim UC due to the COVID-19 pandemic, are a demographically distinct group. In particular, new UC claimants were more likely to be earning higher wages and more likely to have savings.[v]

It should be noted that it is possible that a small number of new UC claimants moved off UC at a later point, with some of the improvement in position of new UC claimants being affected by this.

Actual financial situation

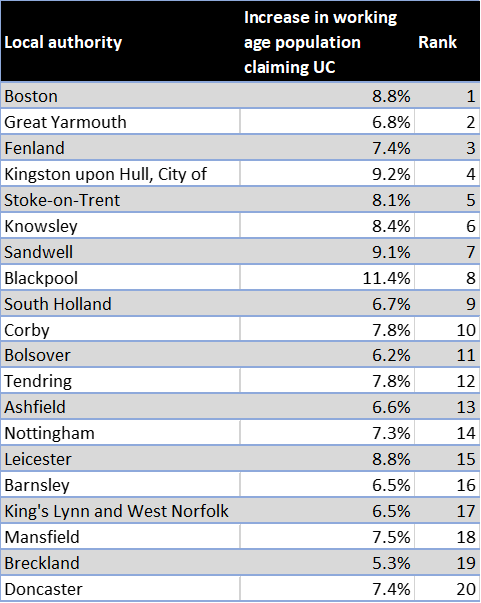

We begin by finding that a significant minority of both existing and new UC households were reporting not being up to date with household bill payments throughout the pandemic, as shown in Chart 1 below.

While the number of non-UC respondents who report not being up to date has remained steady between 2018-19 and May 2020 (5% and 6% respectively), we do find a notable increase in this financial problem among existing UC claimants, rising from 25% in 2018-19 to 41% in May 2020. This changed to 34% in July 2020, rose to a high of 46% in November 2020, and then fell to 38% in March 2021, highlighting the large extent to which existing UC claimants continue to face issues with household bills.

On the other hand, while a relatively high proportion of new UC claimants report not being up to date with at least some household bills near the start of the pandemic in May 2020 (32%), this declined to 19% in July 2020, remained at 20% in November 2020 and then went to 17% in March 2021, indicating that new UC claimants were less likely to face this specific financial challenge as the pandemic continued.

The difference between existing UC claimants and non-UC respondents reporting not being up to date with at least some household bill payment rose by 14 percentage points between before the pandemic (2018-19) and March 2021. Similarly, the difference between existing and new UC claimants rose by 11 percentage points between near the start (May 20) and the later stages of the pandemic (March 2021).

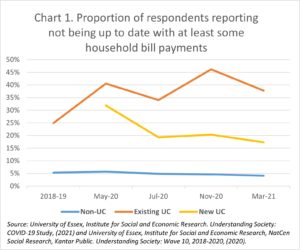

We then focused on an even more specific financial challenge: the proportion of respondents who report not being up to date with housing payments (for example, rent or mortgage) currently[vi], as seen in Chart 2 below.

We once again, unsurprisingly, find a large gap between the experience of UC claimants and non-UC respondents. While only 7% of non-UC respondents in 2018-19 report falling behind on housing payments, this rises to 27% among existing UC claimants. The gap narrows slightly during the early stages of the pandemic, as 6% of non-UC respondents and 20% of existing UC claimants report not being up to date with housing payments in May 2020.

Despite the Government increasing the housing element of UC to ensure it matches at least the 30th lowest percentile of rents in the local area at the start of the pandemic[vii], a notable minority of existing and new UC claimants report not being up to date on housing payments during the pandemic. For existing UC claimants, between 18% and 26% report facing this financial challenge between May 2020 and March 2021, with slight variation and a peak in November 2020 during the first year of the pandemic. On the other hand, 16% of new UC claimants in May 2020 and 23% in July 2020 report not being up to date with housing payments, but there is a notable decline to 18% in November 2020 and 11% in March 2021.

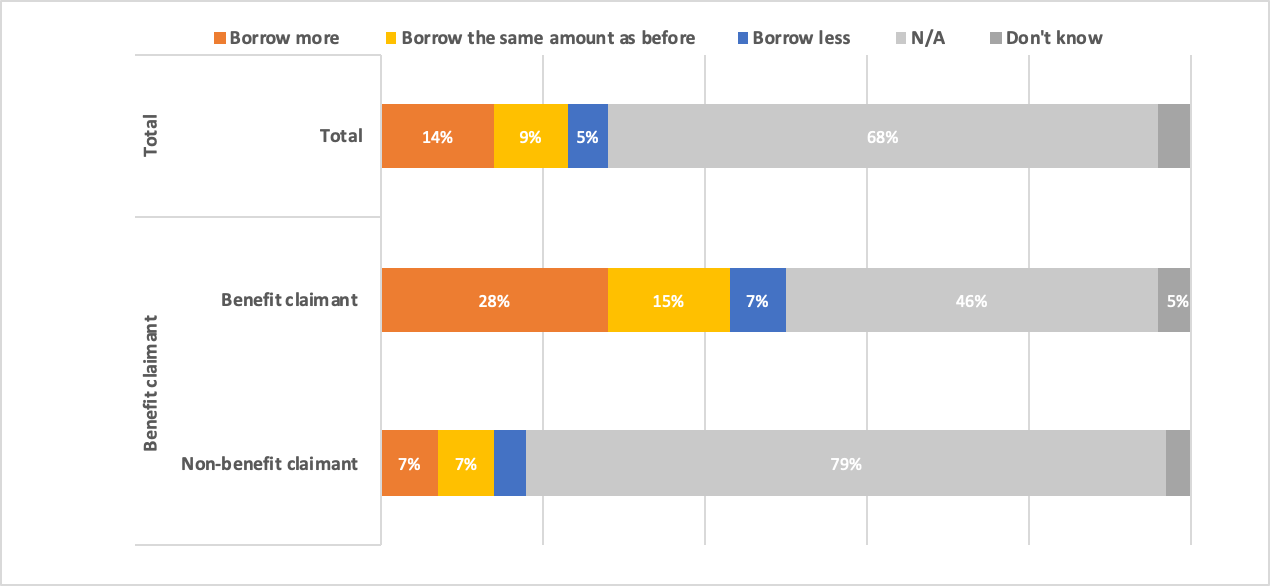

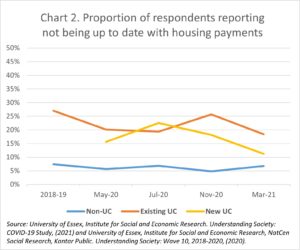

We then examined the proportion of respondents who, during the pandemic, reported changes in their personal debt over the last four weeks, as shown by Chart 3 below.

First, we find that among all population groups and during all time periods, the majority of people’s debt levels has stayed the same. However, what is notable is that both non-UC respondents and new UC claimants were more likely to be decreasing the size of their debt than increasing it at different points of the pandemic. Meanwhile, existing UC claimants were more likely to face a worsening than an improving financial situation in the initial part of the pandemic, with 30% reporting increasing the size of their debts compared to 13% decreasing it in July 2020. However, the number of existing UC claimants who were still increasing their debt fell to 12% by March 2021, but a much higher proportions of 21% of existing UC claimants reported decreasing their debt by March 2021.

Perceived financial situation

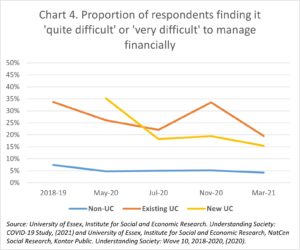

We then examine people’s subjective perceptions of how they are managing financially currently, finding that there have been some notable changes in this perception as the pandemic progressed, as Chart 4 shows below. This chart shows the proportion of respondents finding it difficult (‘quite’ and ‘very’ difficult) to manage financially.

Unsurprisingly, we find a major gap between the number of non-UC respondents and UC claimants both in 2018-19 (7% vs 34% respectively) and near the start of the pandemic in May 2020 (5% vs 26% respectively) who report this, highlighting that a significant minority of UC recipients have continued to struggle financially.

However, we find that there was a slight decrease in number of existing UC claimants who report finding it difficult to manage financially within the initial months of the pandemic, with this seeing a decline from 34% in 2018-19 to 26% in May 2020 and 22% in July 2020, before rising back to 34% in November 2020, and then falling back considerably to 19% in March 2021.

On the other hand, the number of new UC claimants who find it difficult to manage financially starts relatively high (35%) in May 2020, indeed higher than existing UC claimants, but notably declines in the following months, falling to 18% in July 2020, 19% in November 2020 and then 15% in March 2021.

Interestingly, the difference between existing UC claimants and non-UC respondents finding it difficult to manage financially declined by 11 percentage points between before the pandemic (2018-19) and March 2021. Similarly, the difference between new UC claimants and non-UC respondents declined by 19 percentage points between near the start (May 20) and the later stages of the pandemic (March 2021).

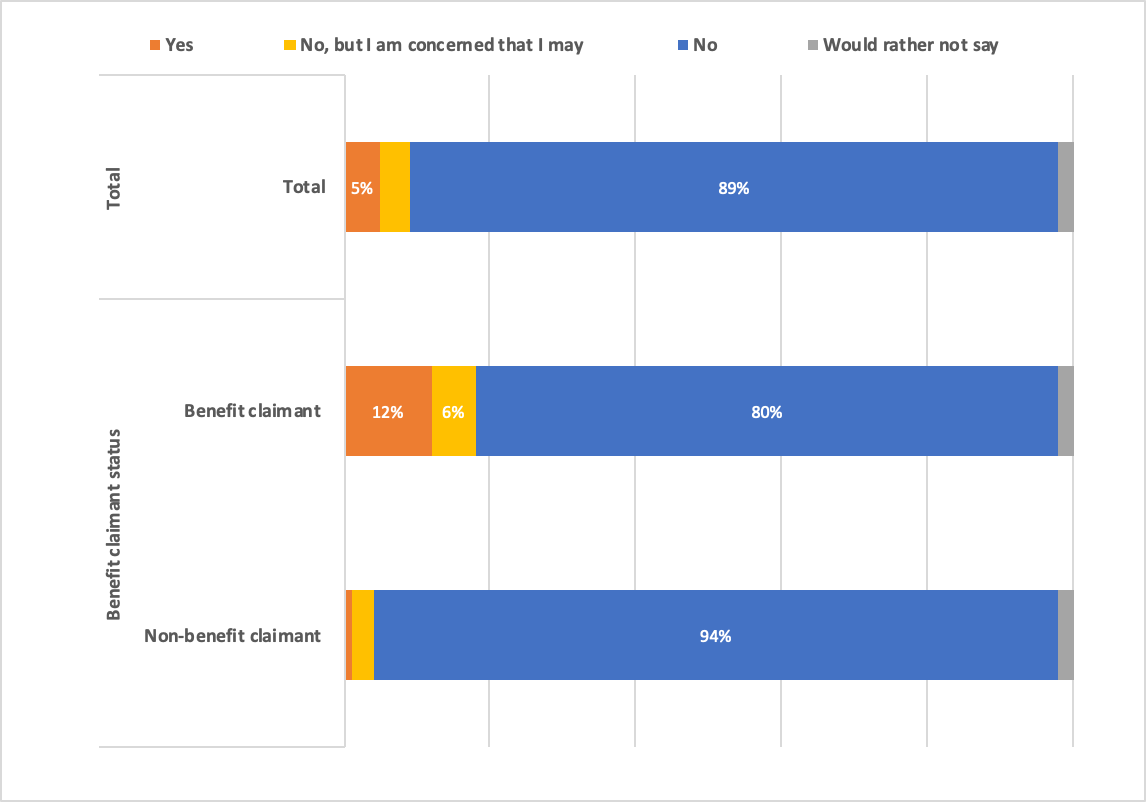

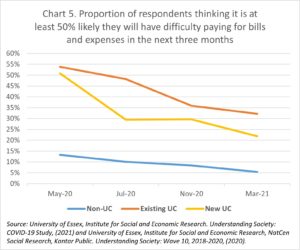

Turning to future perceptions of finances, we find a notable improvement over the course of the pandemic in all people’s perceptions, as shown in Chart 5 below. This is somewhat unsurprising, since other findings in this analysis point to, with some fluctuation, the financial situation of both existing and new UC claimants improving throughout the pandemic.

We find that negative perceptions of future finances are much more common among both existing and new UC claimants than non-UC respondents throughout the pandemic, especially close to the start of the pandemic in May 2020, when only 13% of non-UC respondents expressed this, as opposed to majorities of 54% of existing and 51% of new UC claimants, highlighting the much higher degree of financial uncertainty UC claimants have faced.

While both existing and new UC claimants are much more likely to think there is a major chance they will have difficulty paying for bills and expenses in the next three months, this perception does decline from the early months of the pandemic, falling from 54% to 32% among existing UC claimants between May 2020 and March 2021 and from 51% to 22% among new UC claimants in the same time period. The decline in anxiety around future finances appears to have happened more quickly among those who are new UC claimants.

Notably, the difference between the number of existing UC claimants and non-UC respondents finding it at least 50% likely they will have difficulty paying for bills and expenses in the next three months declined by 14 percentage points between May 2020 and March 2021. Similarly, the difference between new UC claimants and non-UC respondents declined by 21 percentage points May 20 and March 2021.

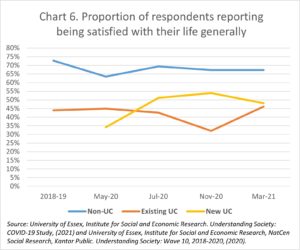

Finally, we have also examined broad life satisfaction of UC claimants during the pandemic, as shown in Chart 6 below.

Several interesting trends emerge when we look specifically at the respondents who report feeling satisfied. First, it should be noted that even before the pandemic, there was a significant gap in life satisfaction between non-UC respondents (73%) and existing UC claimants (44%), as would be expected.

Second, while life satisfaction did fall in May 2020 for people who are not UC claimants relative to the responses given in 2018-19 (73% to 64%), the same fall did not occur for existing UC claimants (44% to 45%) at the start of the pandemic.

Third, while new UC claimants were slightly less likely to report being satisfied than existing UC claimants in May 2020 (34% vs 45%), this trend reversed as the pandemic continued and by November 2020, a majority (54%) of new UC claimants report being satisfied, as opposed to 32% of existing UC claimants. However, the two groups moved closer, so that by the later stage of the pandemic in March 2021, 46% of existing and 48% of new UC claimants reporting being satisfied with their life.

Conclusion

First, it is vital to highlight that our analysis shows that significant minorities of both existing and new UC claimants faced major difficulties in their financial situation throughout the first year of the pandemic, and were much more likely to face these issues than the rest of the public, despite the increase in government support provided through working age benefits.

Second, the situation for existing UC claimants has shifted throughout the pandemic, with some evidence for improvement relative to non-UC respondents as the pandemic progressed, especially by March 2021. The picture is more mixed relative to 2018-19, with existing UC claimants seeing a variety of differences in their actual and perceived financial difficulties.

Third, it is notable that while new UC claimants were facing actual and perceived financial difficulties at a similar rate to existing UC claimants closer to the start of the pandemic in May 2020, they were more likely to experience a notable improvement in their financial situation as the pandemic continued, and by November 2020, new UC claimants were less likely to express having several types of financial difficulties than existing UC claimants. However, the gap appears to narrow in actual and received financial situation by the later stages of the pandemic in March 2021.

References

[i] Matthew Whittaker, “Paying for the pandemic: the economic consequences of COVID-19”, The Health Foundation, https://www.health.org.uk/news-and-comment/blogs/paying-for-the-pandemic-the-economic-consequences-of-covid-19, 2021.

[ii]

Institute for Fiscal Studies, “Spending and saving during the COVID-19 crisis: evidence from bank account data”, https://www.ifs.org.uk/publications/15146, 2020.

[iii]

University of Essex, Institute for Social and Economic Research. Understanding Society: COVID-19 Study, (2021). [data collection]. 4th Edition. UK Data Service. SN: 8644, 10.5255/UKDA‐SN‐8644‐4.

[iv]

University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 10, 2018-2020, (2020). [data collection]. 13th Edition. UK Data Service. SN: 6614, http://doi.org/10.5255/UKDA-SN-6614-14.

[v]

Peabody, “Credit where it’s due? Claiming Universal Credit during the COVID-19 pandemic”, https://www.peabody.org.uk/media/14903/universal_credit_34.pdf , (2021).

[vi]

*2018-19 respondents were asked a slightly different question: whether they were not up to date on housing payments in the last 12 months.

[vii]

HM Treasury,“The Chancellor Rishi Sunak provides an updated statement on coronavirus”, https://www.gov.uk/government/speeches/the-chancellor-rishi-sunak-provides-an-updated-statement-on-coronavirus# (2020).

[Image:

Tierra Mallorca]