Summary

This report offers compelling principles and consequent policy ideas for an ambitious agenda of tax reform that tackles the leading economic, social and environmental challenges of the 2020s and beyond.

It is the final vision that flows from our multi-year project on tax reform, which has been advised by a high-profile cross-sector, cross-party commission.

The Government recently launched its 2022 Spring Statement Tax Plan, which has been described as the foundations of a future low tax economy. But we believe the Chancellor can be and should be much more ambitious with tax reform during this Parliament.

Thus, to build on this Government’s ongoing thinking about tax in the years ahead, we propose nine key principles that should underpin an ambitious programme of tax reform, supported by policy recommendations to achieve them.

- Supports effort, enterprise and entrepreneurialism

- Fairly taxes income derived from luck, rent-seeking and externalities

- Treats similar activities by individuals and institutions more equally

- Incentivises investment to facilitate long-term economic growth

- Ensures sound public finances

- Protects and enhances the livelihoods of the poorest

- Is easier to understand and more difficult to avoid

- Supports the transition to a net-zero economy

- Helps to address regional imbalances, thereby levelling up the country

This final paper includes only policies that derive directly from reports we commissioned for our project on property, carbon, work and wealth, and business taxation.

Introduction

The past two years have been tumultuous. The world has been rocked by multiple major crises, from the COVID-19 pandemic to the war in Eastern Europe. Divisions in and disruptions to our society and economy have been exacerbated.

The UK economy is now in a fragile state. There is record, rising inflation which is eroding livelihoods.[1] Long-term growth is forecast to remain modest at best.[2] Net public debt and the structural budget deficit are at historic highs, thanks to record levels of public spending necessary to combat the consequences of Coronavirus.[3] The sustainability of the UK’s fiscal position is vulnerable to rising interest rates.

The UK Government has, rightly, committed to three preeminent objectives in the years ahead: economic, social, and environmental. Boosting growth and living standards after the pandemic. Levelling up the country to improve opportunities and outcomes for those living in so-called ‘left-behind’ communities, thereby reducing the geographic inequality which has been particularly pronounced in the UK for too long. And, finally, deeply decarbonising across economic sectors so the UK achieves net zero greenhouse gas emissions by 2050, so as to avoid the most extreme and expensive consequences of rapid climate change.

Despite the uncertain economic and fiscal outlook after the pandemic, this current Conservative Government has committed to increased levels of public spending to achieve these three major objectives. Unusually for a Conservative Government, there is a high degree of tolerance for ongoing historically high levels of taxation and spending. This is a very different situation to after the 2008 financial crisis, when the Conservative-led Coalition Government that came into power cut both taxes and spending, the latter deeply.

Certainly, the traditional centre-right approach to taxation is largely sceptical. The instinct of centre-right politicians and policymakers is to pursue a tax cutting agenda, stemming from a belief in personal responsibility, economic freedom and a smaller state. Indeed, the Chancellor recently announced the Spring Statement Tax Plan, with a vision for a lower tax economy that helps families with the cost of living, boosts growth and productivity, and lets people keep more of what they earn.[4] This seemed to mark a return to conventional Conservative thinking, but in reality official Government policy is still consistent with a more social democratic model.

The truth is that, in a mature economy, governments play a major role in ensuring both efficient and equitable outcomes. As the philosopher Professor Steven Pinker has noted: “The number of libertarian paradises in the world – developed countries without substantial social spending – is zero”.[5] What’s more, there seems little public appetite or institutional capacity for the degree of spending cuts experienced in the 2010s.[6] As such, the centre-right cannot simply look only to slashing taxes.

If high levels of public spending to meet major objectives are to be maintained whilst servicing current budget surpluses, in the 2020s this country will need to pursue a tax reforming – not solely a tax cutting – agenda. Indeed, as well as shoring up the public finances, tax reform can also play a positive part in supporting the Government to achieve their leading economic, social and environmental objectives.

Reforms to taxation, nevertheless, can be incredibly politically contentious. This causes conservatism in the way HM Treasury approaches tax as a policy lever, meaning it is under-utilised as a tool to help achieve positive, far-reaching change.

But if tax reforms are to be suitably effective and ambitious, as they should and can be, then it is vital that policy proposals derive from clear principles that attract sufficient political support.

For the past two years, the team behind Bright Blue’s project on tax reform – advised by a cross-sector, cross-party commission – has sought to do exactly this.

Our project

The purpose of our project has been to generate compelling principles and consequent policy ideas for an ambitious agenda of tax reform that tackle the leading economic, social and environmental challenges of the 2020s and beyond.

To arrive at the principles and policies in this final report, we undertook four main activities.

First, we established and hosted several meetings of a high-profile, cross-sector, cross-party commission to generate and exchange ideas.

The members of this commission included:

- The Rt Hon David Gauke, Former Secretary of State for Justice

- The Rt Hon Sir Vince Cable, Former Secretary of State for Business

- The Rt Hon Lord Willetts, President of the Advisory Council and Intergenerational Centre at the Resolution Foundation

- The Rt Hon Dame Margaret Hodge MP, Former Chair of the Public Accounts Committee

- The Rt Hon Andrew Mitchell MP, Former Secretary of State for International Development

- James Timpson OBE DL, Chief Executive of the Timpson Group

- Luke Johnson, Entrepreneur and Chairman, Risk Capital Partners

- Emma Jones MBE, Entrepreneur and Founder, Enterprise Nation

- Mike Cherry OBE, National Chairman, Federation of Small Businesses

- Mike Clancy, General Secretary, Prospect trade union

- Victoria Todd, Head of the Low Incomes Tax Reform Group

- Sam Fankhauser, Professor, University of Oxford

- Christina Marriott, Interim Director of Policy and Advocacy, British Red Cross

- Helen Miller, Deputy Director and Head of the Tax Sector, Institute for Fiscal Studies

- Giles Wilkes, Former Special Adviser, Number 10 Downing Street

- Caron Bradshaw, CEO, Charity Finance Group

- Pesh Framjee, Global Head of Social Purpose and Non Profits, Crowe UK

- Robert Palmer, Director, Tax Justice UK

- The Rt Hon Lord Adebowale CBE, Chair, Social Enterprise UK

Second, we conducted an extensive literature review of existing UK and international evidence on taxation, to examine where the UK’s approach to domestic and international taxation is currently failing, identify alternative effective policy approaches from overseas, and ascertain what principles should underlie a program of ambitious, strategic reform of taxation.

Third, we conducted an extensive stakeholder consultation with current and former politicians, special advisers, civil servants, experts from the tax sector, academics, and senior representatives from the private, public and third sectors to learn about and appraise the UK’s current tax system, as well as identify a wide pool of new principles and policies to reform the tax system.

Fourth, we commissioned independent experts to author reports, and propose policies within them, on property, carbon, work and wealth, and business taxation. All these reports have been published over the past year.

This final paper includes only policies that derive directly from these commissioned reports. So, the proposed policies are not intended to be exhaustive and should not be treated as such. They are meant to be examples of some policies that fit with the principles we have generated. There will be many other compelling policy ideas – from a range of individuals and organisations – that should be adopted by the UK Government.

It is also very important to emphasise that members of the commission, although influential in the development of the principles and policies, do not necessarily endorse all of them.

Our principles for tax reform

The Government recently launched its Spring Statement Tax Plan[7], which has been described as the foundations of a future low tax economy. That Spring Statement Tax Plan reveals a determination by the Chancellor to lower taxes to help families with the cost of living, boost growth and productivity, and let people keep more of what they earn.

But we believe the Chancellor can be and should be much more ambitious with tax reform during this Parliament. The Chancellor’s Tax Plan should be supplemented: to not just always ideologically fixate on lowering taxes, and to also use tax as a tool to help a much wider set of economic, social and environmental goals. Ultimately, we believe that tax can achieve its potential as a substantial policy lever than facilitates bigger and bolder changes to our socioeconomic model than it does at present.

Thus, to build on this Government’s ongoing thinking about tax in the years ahead, we propose nine key principles that should underpin an ambitious programme of tax reform, supported by policy recommendations to achieve them.

1. Supports effort, enterprise and entrepreneurialism

2. Fairly taxes income derived from luck, rent-seeking and externalities

3. Treats similar activities by individuals and institutions more equally

4. Incentivises investment to facilitate long-term economic growth

5. Ensures sound public finances

6. Protects and enhances the livelihoods of the poorest

7. Is easier to understand and more difficult to avoid

8. Supports the transition to a net-zero economy

9. Helps to address regional imbalances, thereby levelling up the country

Supports effort, enterprise and entrepreneurialism

Supports effort, enterprise and entrepreneurialism

Effort, enterprise and entrepreneurialism are all essential ingredients to achieve economic growth, which is an imperative as we emerge from the Covid-19 pandemic. Fortunately, GDP has now surpassed its pre-pandemic level[8] and the most recent unemployment rate matches record lows.[9] But economic growth forecasts for the years ahead – including from the Office for Budget Responsibility (OBR) – remain modest, from a both historical and international perspective.[10] This country also now faces significant economic problems, especially record, rising inflation.[11] Doing much more to encourage productive activity will in, the near-term, power economic growth to tackle our growing economic problems. In the long-term, it will boost Britain’s notorious sluggish productivity.

More than this, there is a moral imperative for encouraging such activity. Effort is associated with a more productive economy, a societal benefit, but it can also engender greater feelings of agency and accomplishment, benefitting individuals. Entrepreneurialism often involves considerable risk-taking, but can yield substantial private and public rewards in the long-run. Our society prizes deeply the principle that rewards should be linked to effort; it is essential for believing the socio-economic system is fair. So effort, enterprise and entrepreneurialism are morally and economically important activities, which should be encouraged by the tax system as far as possible.

This Conservative Government is increasing the National Insurance (NI) headline rate through the new Health and Social Care Levy (HSCL), while planning to reduce the basic rate of Income Tax from 2024-25.[12] This means that tax in this country is increasingly falling on income from work rather than income from other activities. It should be an urgent priority to better reward people’s effort by reducing taxes on work, especially NI and the HSCL.

There are ways of doing exactly this in a way that would both help businesses to minimise their costs in the short-term and, in the long-term, feed through into people’s wages and allow them to keep more of the money they earn from a job, all of which is important when inflation is increasing sharply. Reducing the rate of the new HSCL and NI more generally, and broadening their scope to other forms of income, would spread the impact of these taxes more evenly across the income and age distribution, reversing the troublesome shift of overall tax onto workers.

There is also more that the tax system can do to support enterprise and entrepreneurialism. The Enterprise Investment Scheme (EIS), Seed Enterprise Investment Scheme (SEISSs) and Venture Capital Trusts (VCTS) are important parts of the tax system that support innovative start-ups. Social Investment Tax Relief (SITR) is important to ensure social enterprises scale up and deliver value for their communities. But at present, these reliefs suffer from poor promotion and long delays.[13] For start-ups with limited access to capital, delays can have a damaging impact, forcing them to delay hiring or in some cases, pause vital projects.

The Government could better support effort, enterprise and entrepreneurialism in a number of ways, including these policy ideas:

- Prioritise significantly lowering the headline rate of the employer element of the HSC Levy from 1.25% on income above the existing employer NICs threshold as soon as possible. Then, if the public finances allow, the rate of employers NICs should then also be cut. This measure would represent a cost to the Treasury in the short term. However, falling employer NICs, initially with the HSC Levy, can be expected to result in greater employment, higher wage levels and/or more profitable businesses in the long-term.

- The HSCL should be broadened to apply to pensions and rental income. Broadening the scope of the HSCL would enable the rate of the HSC Levy and NI to be cut and ensure revenue for health and social care is raised in a way that spreads the burden of the new tax more equally across society.

- End the exemption from Class 1, 2 and 4 NICs for those working above the State Pension Age. Exempting those above the SPA from NICs ignores a long-term increase in people working past retirement age. Extending Class 1, 2 and 4 NICs to those above the SPA will contribute to raising revenue to offset the reduction in the rate of the HSC Levy and NI.

- Venture capital reliefs such as Enterprise Investment Scheme (EIS), Seed Enterprise Investment Scheme (SEIS) and Venture Capital Trusts (VCTs) should be maintained at current levels and the process for qualifying and accessing these reliefs should be streamlined in line with the Office for Tax Simplification’s proposals. These include administrative changes such as allowing applicants to save partially completed forms online, alongside allowing investors to benefit from the Capital Gains Tax (CGT) relief in years where they make an income tax loss.

- Social Investment Tax Relief should be preserved, but more resources should be invested in promoting the relief. There is a sound economic rationale to allow investors in social enterprises to benefit from reliefs similar to the venture capital reliefs. However, to ensure the relief’s long-term viability, more needs to be done to combat low levels of awareness among accountants and social enterprises.

Fairly taxes income derived from luck, rent-seeking and externalities

Fairly taxes income derived from luck, rent-seeking and externalities

Profit-making derived from effort, enterprise and entrepreneurialism is economically and socially good. But returns and profits do not always come from these productive activities. Sometimes, they can arise from sheer luck – such as happening to hold shares in a digital company right before the pandemic or inheriting a large sum from your family. Businesses can wield monopoly power to acquire higher than normal returns. Individuals and businesses may profit from activities that cause wider damage, such as pollution, without shouldering enough of the cost. In many ways, the tax system does not adequately tax income derived from these sources. Indeed, if it did, it could lower taxes on effort, enterprise and entrepreneurialism in a more sustainable manner.

First, luck. One of the key trends of the past three decades has been a large and sustained increase in wealth, levels of which have risen from 300% to 700% of GDP since the 1990s. Much of this can be attributed to rising asset prices. This has been largely underpinned by a global and long-term fall in interest rates; put another way, those who held interest-rate sensitive assets at the right time have seen a windfall as interest rates have sharply fallen in recent decades. It is difficult to see why returns based merely on good fortune should attract a significantly lower tax rate, as they do in the UK through Capital Gains Tax (CGT), than for other kinds of economic activity.

For children of parents who have accumulated wealth, they are often fortunate to receive financial support through gifts and inheritances that gives them proven advantages in education and employment. Indeed, inheritances can boost lifetime incomes significantly – by as much as 29% for those with wealthy backgrounds, according to the Institute for Fiscal Studies.[14] The current design of Inheritance Tax – with exemptions for gifts made more than seven years before death, and generous reliefs on business and agricultural property – means that many life-enhancing transfers of wealth go untaxed.

Second, rent-seeking. Some can use monopoly power, firm-specific capital, regulatory capture or luck to drive up profits. Here, financial returns take place regardless of effort, enterprise or entrepreneurialism. The excess profit from such activity is known as ‘economic rent’. Taxes on economic rent do not affect investment decisions and behaviour to the same extent that ungenerous taxes on effort, enterprise or entrepreneurialism do. Business taxes in particular should, where possible, focus on economic rent rather than marginal investment and risk.

Third, externalities. The most egregious is the under-pricing of carbon emissions in markets, given the scale of the challenge posed by climate change – which, if not controlled, will result in catastrophic and potentially irreversible effects on the natural environment and society. Overall, to achieve the UK’s legally binding target of net zero emissions by 2050, the amount of taxation on carbon-intensive production and consumption will have to increase, especially in key economic sectors. While a uniform carbon price would disproportionately impact certain economic sectors, it is nevertheless the case at present that the distribution of carbon taxation across the economy is grossly inconsistent and inadequate. The cost of emitting a tonne of CO2 from a car is around £109; aviation, meanwhile, effectively receives a subsidy of around £26.[15]

The flipside of rewarding productive activities in the tax system is fairly taxing unproductive or harmful activities. This could be achieved, to some extent, by some new policies:

- Narrow the gap in headline rates between Capital Gains Tax (CGT) and Income Tax. Two main rates for all capital gains of 18% at the basic rate and 28% at the higher rate ought to be established, with modifications only for assets that have already paid Corporation Tax. This would end the distinction between standard CGT rates and rates applied on residential property or carried income, as well as end Business Asset Disposal Relief and Investors’ Relief. While this approach would narrow, and not eliminate, the discrepancy in tax rates between CGT and Income Tax, it would represent a simplification compared to the current system.

- Replace Inheritance Tax with a Lifetime Receipts Tax (LRT). The LRT should have a starting lifetime allowance of £125,700. The headline rates should mirror Income Tax rates from now, with the threshold set at ten times the Income Tax salary thresholds. A tax that applies to lifetime gifts, and not just gifts bequeathed after (or near) death, would end the arbitrary distinction between the timing of gifts. This would also reduce the abilities of wealthier estates to minimise effective tax liabilities, thereby ensuring that inheritances are taxed more progressively.

- Business Rates should be replaced with a Business Land Tax levied on commercial landowners, based on unimproved land values. This would move the Business Rates system away from taxing investments in commercial property, and focus the tax squarely on the economic rent flowing from the value of unimproved land.

- Set a ‘target price range’ for carbon taxes across the whole economy by 2030. The range should include a 2030 ‘floor price’ that each economic sector would have to achieve at a minimum. A target price range for the economy would be a significant step towards a coherent carbon taxation framework that reflects the societal cost of emissions. But despite the need for consistency, different sectors will face different challenges in reaching the target price range, hence why a standard, economy-wide tax should be avoided. Indeed, a ‘price floor’ would ensure some flexibility for economic sectors.

Treats similar activities by individuals and institutions more equally

Treats similar activities by individuals and institutions more equally

The current design of the tax system leaves individuals and institutions receiving the same amount of income paying vastly different effective tax rates, significantly distorting the economy.

In regards to individuals, self-employed people pay considerably less in tax than workers. In large part, this is due to there being no equivalent to employers’ NICs for the self-employed. As such, businesses have an incentive to contract labour on a self-employed basis in order to minimise tax liabilities. Individuals, especially younger and affluent ones less dependent on state benefits, also have a tax incentive to supply their labour as a self-employed contractor, rather than as an employee.

Another discrepancy is between those deriving income from assets and those who earn income through work: the former pays proportionately less tax than the latter. As an example, someone might be an owner-manager of their own business and take their income as dividends or retain income in the company and take it later as capital gains. Both of these forms of remuneration are more lightly taxed than labour income, which is subject to higher Income Tax and NICs rates.

Indeed, we can observe starkly different overall tax rates for individuals depending on how they take their income. Among very high earners, those earning £100,000 or more, some pay average tax rates of close to 10% – largely driven by the 10% rate on capital gains qualifying for Entrepreneur’s Relief – while others pay close to the headline 45% Income Tax rate.[16]

Institutions that are otherwise similar also face arbitrary distinctions in the way they are taxed. Because interest is tax deductible, investments that are financed through debt are treated differently to investments financed through equity.[17] The result is that projects funded through equity require a higher rate of return to be viable than those financed through debt. Businesses should not face a penalty or advantage based on how they choose to finance their investments.

More thought also needs to be given to bricks-and-mortar businesses versus online businesses, where the former pay more in Business Rates than the latter. Large differentials in Business Rates bills are not necessarily sufficient grounds to create a special tax on online retailers; Business Rates fall mostly, if not entirely, on commercial landlords, and as such only advantage online retailers in the short-term. There may, however, be other justifications for singling out online retailers. Many of the largest online retailers are able to take advantage of profit-shifting to other jurisdictions overseas to reduce tax burdens, which gives them a tax advantage over bricks-and-mortar businesses. The UK should be at the forefront of global efforts to respond to profit-shifting and tax multinational enterprise more fairly and robustly.

There is an economic rationale for reducing the gaps in effective tax rates for otherwise similar individuals and institutions. Doing so would reduce the distortions currently present in the tax system that favour some activities over others. And it would reduce the incentives for individuals and businesses to artificially package their activities in order to lower their tax rate.

At a moral level, reducing such gaps would make the tax system seem fairer. It is not clear why the hard work of an employer, asset manager or self-employed contractor should be rewarded more than the hard work of an employee. Nor is it clear why businesses should pay different amounts of tax merely because of their financing arrangements or business model.

It is therefore important, both for economic and moral reasons, to lessen the differences in tax rates between different legal forms of income and businesses. This does not need to mean complete parity: there are still differences between the nature of different forms of work such as employment and self-employment, and in some cases – such as with individual investments – we do not want to discourage entrepreneurialism and risk-taking. But the scale of current gaps between these different legal forms in the UK cannot be justified.

To narrow the gap in the tax take between different individuals and institutions receiving the same income, the Government as a first step should:

- Prioritise significantly lowering the rate of the employer element of the HSC Levy from 1.25% on income above the existing employer NICs threshold as soon as possible. Then, if the public finances allow, the rate of employers NICs should then also be cut. Focusing on employer NICs – which are ultimately borne by employees through lower wages – would reduce the effective difference in tax rates between employees and the self-employed. Employer NICs account for most of the difference in effective tax rates between the two, as there is no equivalent for employer NICs for self-employed workers.

- Narrow the gap in headline rates between Capital Gains Tax (CGT) and Income Tax. Two main rates for all capital gains of 18% at the basic rate and 28% at the higher rate ought to be established, with modifications only for assets that have already paid Corporation Tax. This would narrow, but not eliminate, the gap in headline rates between CGT and Income Tax. As such, it would weaken the tax incentives to convert income to capital gains, and ensure that the capital gains and income from work are more similarly taxed.

- Eliminate the bias in favour of debt-financed investment by excluding interest from the corporate tax system. The cause of the debt-over-equity bias within our corporate tax system is that payments to holders of debt can be deducted, but the real return necessary to compensate shareholders for providing equity is not. One way to reduce the tax bias in favour of debt would be to effectively exclude interest from the tax system altogether. Debt interest payments would no longer be deductible expenses, but interest payments received would not be taxed either. This would bring the marginal effective tax rate on debt financed investments in line with the marginal effective tax rate on equity financed investments.

- The UK should lobby internationally for the OECD’s proposed agreement on a 15% global minimum corporate tax to use a cashflow base. At the G7 summit in 2021, agreement was reached on a 15% global minimum corporate tax rate for large multinationals. Lobbying for the global minimum tax to have a cashflow base would ensure tax competition is focus on pro-investment and positive-sum reforms to the tax base. This aspect would better align the global minimum corporate tax with the goal of raising more revenue from highly profitable large multinationals., and ensure tax revenue from online companies and bricks-and-mortar companies is narrowed.

Incentivises investment to facilitate long-term economic growth

Incentivises investment to facilitate long-term economic growth

Investment from individuals and businesses is key to building a dynamic, productive and prosperous economy. Investment interacts in many ways with the tax system, chiefly through Corporation Tax and Business Rates for businesses, and Capital Gains Tax for individuals.

Admittedly, the Government has recognised the role tax policy can play in spurring business investment through policies such as the ‘super-deduction’, which offers businesses a 130% capital allowance against their Corporation Tax liabilities.[18]

Still, Corporation Tax in the UK has one of the least generous systems of capital allowances among OECD countries. Indeed, before the Covid-19 pandemic, only one OECD country – Chile – had a less generous system of capital allowances than the UK.[19] This penalises long-term investments, particularly when it comes to investments in buildings and structures. Moreover, the super-deduction is currently set to end in 2023, meaning that, combined with the scheduled rise in headline Corporation Tax rates, the corporate tax system is set to become significantly less generous towards investment in the coming years.

Added to this, the treatment of corporate losses, which are currently not adjusted for inflation, is less generous than it could be: due to levels of inflation over the last twelve years, a £100 loss made in 2010 that took ten years to carry forward would lose £24 worth of value.[20] As a result, all things being equal, businesses will prefer safe, short-term investments to risky, long-term investments.

The economic effects of Business Rates can be thought of, conceptually, as a tax on unimproved land value and a tax on improvements to commercial property. Taxes on land value are highly economically efficient; they do not interfere with economic activity as taxing land will not reduce its supply. But through Business Rates, businesses are also taxed for making improvements to their commercial property. This acts as a disincentive for investments to improve infrastructure such as generators, boilers and blast furnaces.[21]

Currently, for individuals, a lower rate of Capital Gains Tax (CGT) and tax-free initiatives such as Individual Savings Accounts (ISAs) exist to promote individual investment. But CGT chips away at the normal returns to investment by taxing gains arising only from inflation. At present, a person could make an investment that performed equal to inflation, and get taxed on the nominal returns, making them worse off than they were before investing. It is only fair that, if the upsides of investments are rightly taxed more, more is done to mitigate against the potential downsides.

There are many tax reforms that the Government could take to make investment more attractive, including:

- Move to the full immediate expensing of capital investment in new plants, machinery, and industrial buildings when the investment super-deduction expires in 2023. Investment in new plants and machinery would be treated in the same way as any other business expense. Moving to full expensing permanently after 2023 for all capital investment would reduce the marginal effective tax rate for investment to zero. It would, in effect, eliminate the tax bias against investment. This would be a significant tax reduction on investment, reducing long-run corporate taxes revenues on a static basis. But this would be offset by higher tax revenues elsewhere resulting from higher output.

- Allow corporate losses to be carried forward with a factor that adjusts for inflation and a safe rate of return on capital. The 50% annual cap of loss carryforwards should also be eliminated. Although losses can be carried forward and offset against future tax returns, inflation and the time value of money erode the value of the tax losses. This creates a bias towards lower risk investments and distorts firm behaviour. Allowing firms to preserve the present discounted value of losses would encourage investment and risk-taking.

- Business Rates should be replaced with a Business Land Tax levied on commercial landowners, based on unimproved land values. Currently, Business Rates can be conceptualised as a combination of a highly efficient tax on unimproved commercial land and a distortive tax on improvements to commercial property. By shifting the tax burden away from investment and towards unimproved land, this proposal would have a positive impact on productivity and, in turn, wages.

- Reintroduce inflation indexation on CGT liabilities. Given the behavioural impacts that a rise in CGT rates could have on individual investment and on tax revenues, rate rises should be paired with offsetting measures that improve the design of the tax base to protect the real value of investments.

- Allow capital losses to be carried back for up to three years and set against taxable income, with relief restricted to CGT rates. Individual investors are only able to set capital losses against capital gains in the current tax year, or carry them forward to future tax years. In principle, there is no reason why capital loss offsets could not be extended to cover a wider range of assets and a wider period. This would better cushion investors against the downside risk of investments.

Ensures sound public finances

Ensures sound public finances

The UK needs to face up to the fiscal challenges ahead. These are the most acute they have been for decades: gross government debt is now more than 100% of GDP, and the structural budget deficit stands in excess of 15% of GDP, up from around 2.6% pre-pandemic.[22] Admittedly, recent inflation has eroded the value of the UK’s national debt. But in the long term, higher national debt leaves the UK vulnerable to interest rate rises.

Simply borrowing more and more to meet today’s spending demands, and thereby ladening future generations with unsustainable levels of debt, is economically and morally unacceptable. A tax-reforming agenda needs to ensure that, overall, the UK’s fiscal trajectory is sustainable.

We do not necessarily advocate for a strictly revenue-neutral approach when reforming taxes. Anyway, this will be difficult to forecast accurately. Proper revenue forecasting would be dynamic not static, as changes to tax prompt changes to behaviour. The issue is that it is hard to accurately predict how individuals and institutions will respond to tax changes, meaning calculating revenue precisely is impossible in advance. Regardless, the overall impact needs to be consistent with sustainable levels of national debt and the ongoing fiscal target to have a structural budget surplus in the near-term.

There are three important considerations when thinking about tax reform and fiscal sustainability.

First, anaemic economic growth, as the UK has experienced for much of the last decade, will worsen our long-run fiscal position. Measures to encourage effort, enterprise, entrepreneurialism and investment should not only be seen as pro-business policies; they should also be seen as an important piece of the puzzle in terms of strengthening the UK’s fiscal position.

Second, borrowing to invest or cut taxes in the present, in some circumstances, can improve the fiscal position by increasing revenues or reducing spending in the long-term. This is particularly important when it comes to climate change, arguably the greatest challenge of this century. The price of inaction today in reducing emissions is higher costs to mitigate worse environmental effects in the future. Indeed, late action to mitigate net zero – waiting until after 2030 – would make public debt as a proportion of GDP 23 percentage points higher than if the UK takes early action and imposes stronger carbon taxes from the middle of this decade, according to the Office for Budget Responsibility.[23]

Finally, value for money in in both spending and tax reliefs should be a key focus, with a drive to cut waste. While direct public spending is often held to a very high standard of scrutiny, the same cannot be said for the UK’s myriad of tax reliefs. Indeed, a large proportion of tax reliefs do not even have discernible objectives and are not assessed effectively – to the extent that some major tax reliefs, such as Employment Allowance, are “almost impossible to evaluate”, according to the Institute for Fiscal Studies.[24] A major focus for ensuring fiscal sustainability should be developing a more rigorous approach to evaluating, and where necessary scrapping, tax reliefs in order to make the tax system as efficient as possible.

To ensure sound public finances, there are a number of changes to tax policy that could help:

- Adopt the German model for scrutinising tax reliefs. Germany legally mandates biannual reviews of corporate tax reliefs based on a standard evaluative framework on a range of metrics including: target accuracy; cost-effectiveness; necessity; and, sustainability.

- The Patent Box, Film Tax Relief and High End TV Tax Relief should be abolished, and the Employment Allowance should be phased out over the next five years. The empirical evidence suggests that, while Patent Boxes do have some impact on international patent transfers, they have no impact on invention. There are better ways of encouraging innovation. Film Tax Relief and High End TV Tax Relief cost significant more than originally forecast, and largely benefit major international companies rather than smaller scale productions. And the little evidence there is on the Employment Allowance suggests it has a limited impact on employment. Ending these reliefs could raise around £5.2 billion.

- Set a ‘target price range’ for carbon taxes across the whole economy by 2030, with a 2030 ‘floor price’ that each economic sector would have to achieve at a minimum. The Government should also publish an annual assessment in the Budget for how each economic sector and sub-sector performs against the carbon tax target. Setting a target price for the whole economy would set a clear fiscal framework for action on net zero, and deliver a clear signal to businesses and individuals of action on climate change. But simply setting a target means little unless there is an assessment of whether progress is being made towards it. Therefore, alongside setting a 2030 target range for each economic sector, the Government should be required to publish a set of metrics for forecasting how each sector and sub-sector of the economy performs against the carbon pricing target.

- Introduce core ‘carbon tests’ as part of the government’s formal impact assessment process to assess changes to any policy that impacts the price of carbon paid by businesses or households. At a minimum, new measures to price carbon should satisfy tests on: impact on carbon price; alignment with net zero target price range; technological readiness; distributional impact; and, economic competitiveness.

Protects and enhances the livelihoods of the poorest

Protects and enhances the livelihoods of the poorest

The escalating cost of living has made life miserable for many of those on the lowest incomes. This year, average real household incomes are forecast to sustain their largest yearly fall on record.[25] Current elements of the tax system are falling short in terms of protecting the poorest households. Future tax measures need to ensure the poorest have their livelihoods enhanced.

To its credit, the Government has taken action to blunt the impact of the new Health and Social Care Levy (HSCL), which is a 1.25% increase to National Insurance on employees, self-employed workers and employers, by raising employees’ Primary Threshold – or Lower Profits Limit for the self-employed – for National Insurance to £12,570 per annum – a measure that makes the impact of the HSCL more progressive and ensures that those earning between £10,000 and around £25,000 per annum will pay less tax on their earnings in 2022-23. But more can and should be done with tax to protect the poorest.[26]

Some elements of the tax system are plainly regressive. Council Tax disproportionately hits those in lower-value houses, who pay more in Council Tax as a proportion of their property value than those in more expensive homes. Even taking into account Council Tax discounts, on average someone living in a £100,000 house pays about 0.7% of that value in Council Tax each year, while someone in a property worth £500,000 pays 0.35% on average, according to the Institute for Fiscal Studies.[27] In large part, this is because of the disconnect between Council Tax bands, which are based on 1991 valuations, and today’s house prices. The Government has already recognised the role Council Tax can play in alleviating costs for struggling households – it introduced a rebate on Council Tax to mitigate against rising energy bills – but this is only a temporary measure.[28]

We must also be mindful of how societal projects can incur costs on individuals. The transition to net zero, which on some figures could cost the UK £1.4 trillion over the next three decades[29], could – without proper public policy – risk being expensive for the poorest in society. High-profile opposition to higher carbon taxes, such as the ‘gilets jaunes’ movement in France, underscore the consequences of not adequately considering this in the development of climate policy.

It is vital to pursue a just transition to net zero. That means those on low incomes do not bear burdensome costs. This is not only morally fair; it is also key to ensuring lasting political support for deeper decarbonisation. It is also entirely feasible; countries such as Sweden, Norway, Japan and France already hypothecate carbon taxes to reallocate a proportion of revenues through rebates, tax cuts and green investment.[30]

There are many areas of tax in which the UK could do more to protect the least well-off. As a first step, the Government should:

- Replace Council Tax and Stamp Duty Land Tax with an Annual Proportional Property Tax (APPT) on the capital value of houses, with a tax exemption for houses worth less than £50,000. Doing this would ensure that property taxes in the UK have an explicit link with today’s house prices. An APPT would also be more progressive with respect to property values than the current Council Tax system.

- Ensure that houses are revalued for tax purposes annually. Or at least on a regular basis, by applying modern statistical techniques to price data to estimate property values. Such an approach is already used in at least 15 other countries. To smooth increases in tax for households, property taxes could be based on a three-year moving average of the property’s value.

- Create a ‘Green Dividend Framework’ made up of the various carbon pricing schemes that contribute to the Exchequer, and identify a specific portion of funds from the revenues to be used to reduce the impact of rising prices on low-income households and vulnerable customers. Beyond the environmental gain, the key societal value of carbon taxation us the revenue it will generate to fund public services and to reinvest in driving the adoption of green technologies. To ensure individuals feel the value of revenue generated more directly, the Government should establish a Green Dividend Framework. This would allow for a total figure to be set for what has been delivered to the public purse, which could be set out in personal tax summaries. While those on the lowest incomes emit the least compared to all other income deciles, a flat carbon tax would disproportionately impact those households. This is demonstrably unfair and can only be avoided if a portion of the revenues generated by a more consistent regime are redistributed to support those most impacted.

Is easier to understand and more difficult to avoid

Is easier to understand and more difficult to avoid

There are often good reasons behind the complexity of the UK’s tax system, which needs to reflect a variety of different circumstances and situations. But a needlessly complex tax system is hard to understand, reducing the transparency of taxes and the ability of politicians to explain what tax reforms are achieving.

There are two ways that we can make the tax system easier for individuals and institutions to understand. First, ensuring that the design of taxes is more explicitly linked to their purpose; in the case of property taxes, for example, there should be more resemblance to today’s house prices.

Second, simplifying reliefs. There has been a proliferation of reliefs and offsets to the tax system, to the extent that HMRC does not even maintain a complete and accurate list of all UK tax reliefs; even among those that are monitored, many lack discernible objectives or the cost of them is not known.[31]

Indeed, in large part due to the extensive range of reliefs, businesses often find navigating the Business Rates system is costly in terms of time and effort: some responses to the Government’s Fundamental Review of Business Rates noted that “complexity in the system can lead to ratepayers failing to understand their eligibility [for Business Rates reliefs], or relying on external agents for support in navigating the system”. Too much complexity can have an impact on productive economic activity.[32]

A further concern is ensuring that taxes are harder to avoid. For individuals, some taxes – particularly Inheritance Tax – are relatively easy to avoid: wealthier estates can take advantage of reliefs on Inheritance Tax, or avoid the tax entirely by passing on assets well before death. Multinational businesses often use profit-shifting to minimise their tax liabilities by moving profits to low-tax jurisdictions overseas. In both cases, this makes the tax system both less effective and less equitable, especially when wealthier individuals and larger companies have access to the advice that can ensure they avoid more tax.

Some policies that the Government can pursue to make the tax system easier to understand, and make taxes harder to avoid, include:

- Replace Council Tax and Stamp Duty Land Tax with an Annual Proportional Property Tax (APPT) on the capital value of houses. Doing this would ensure that property taxes in the UK have an explicit link with today’s house prices, making the system more intuitive for taxpayers.

- Adopt the German model for scrutinising tax reliefs. Germany legally mandates biannual reviews of corporate tax reliefs based on a standard evaluative framework on a range of metrics including: target accuracy; cost-effectiveness; necessity; and, sustainability.

- Replace Inheritance Tax with a Lifetime Receipts Tax (LRT). A tax that applies to lifetime gifts, and not just gifts bequeathed after (or near) death, would end the arbitrary distinction between the timing of gifts. This would also reduce the abilities of wealthier estates to minimise effective tax liabilities, thereby ensuring that inheritances are taxed more progressively.

- Business Property Relief and Agricultural Property Relief in IHT, or the new LRT, should only apply where the donor had a demonstrable working relationship to the business or farm and for at least two years after acquisition. Reliefs for business and agricultural property are there for a good reason: to ensure the viability of family businesses as they are passed down. But they should be better targeted at genuine and viable family businesses. Requiring donors to demonstrate that they owned, worked for, or had significant control in the company or farm, and clawing back relief if the business was sold within two years of acquisition would make sure that these reliefs benefit the group they are supposed to.

Supports the transition to a net-zero economy

Supports the transition to a net-zero economy

Achieving the UK’s legal commitment to net zero emissions by 2050 – meaning that any greenhouse gas emissions the UK does produce by then are offset overall – is the defining and transformative policy goal of this century. Experts have warned that, on a global scale, failing to achieve net zero by 2050 will result in global warming above 1.5 degrees, bringing with it increased risk of irreversible and catastrophic environmental changes, including rising sea levels, loss of ecosystems, and unprecedented flows of migration.[33]

While the key policy drivers of this transition will be investment, innovation and spending, the tax system should nevertheless play a role in supporting the UK’s net zero ambitions.

The new UK Emissions Trading Scheme, a cap-and-trade system which sets a limit on total emissions and creates a carbon market to link emissions to a price signal, is pricing carbon at around £50 per tonne of CO2. But according to Government estimates, prices on carbon may need to rise as high as £125-300 per tonne of CO2 to achieve net zero.[34]

At the moment, the UK’s carbon pricing across different economic sectors is inconsistent and insufficient. Different sectors of the economy are subject to vastly different levels of carbon taxes. The implicit price that taxpayers and consumers pay for emitting a tonne of CO2 can vary by as much as £700, according to the Energy Systems Catapult. If anything, certain sectors such as aviation and residential gas use receive a subsidy for carbon emissions.[35]

The mounting cost of living presents a challenge to the political viability of carbon taxes. Recently, the UK Government has cut Fuel Duty by 5p to support motorists with the rising cost of fuel, which goes against the direction of net zero by further subsidising carbon-heavy activity. In the long term, this is not sustainable for the environment or the Exchequer, since motorists are increasingly shifting to EVs, which are not subject to Fuel Duty. More needs to be done, for transport and beyond, to develop a credible set of reforms to carbon taxes that protects low-income households and builds a lasting political consensus as we make the transition to net zero.

Tax needs to support the UK’s transition to a net zero economy, with some policy ideas including:

- Set a ‘target price range’ for carbon taxes across the whole economy by 2030, with a 2030 ‘floor price’ that each economic sector would have to achieve at a minimum. Setting a target price for the whole economy would set a clear fiscal framework for action on net zero, and deliver a clear signal to businesses and individuals of action on climate change.

- Create a ‘Green Dividend Framework’ made up of the revenues from carbon pricing measures. This would allow for a total figure to be set for what has been delivered to the public purse by carbon taxation measures, and increase transparency around green tax reforms.

- Immediately pilot a voluntary road pricing scheme for all road users ahead of a national rollout from 2030, including ‘Green Miles’ that offer a discount for a period to those driving electric vehicles and on low incomes, as well as surge pricing in congested areas. As drivers switch to electric vehicles (EVs), we need a strategy for replacing the substantial revenues brought in by Fuel Duty. The most viable replacement for Fuel Duty is a road pricing scheme, charging road users on a per-mile basis. Given the danger that the introduction of a road pricing scheme slows adoption of EVs, the Government could introduce a temporary ‘Green Miles’ scheme that offers a proportion of discounted or free miles to those with EVs or on low income. Any road pricing scheme should also include a surcharge for non-residents in urban areas to reduce car use and promote public and active transport.

- Reform Air Passenger Duty so it delivers a more consistent carbon price and offers discounts for ‘Green Miles’ based on the proportion of sustainable aviation used. A frequent flyer surcharge should also be introduced. Air Passenger Duty (APD) should be reformed so it is directly linked to the net zero target, such as through removing the lower rate on short-haul flights or linking charges more directly to distance travelled. To target the scheme at those with the biggest impact, there should also be a surcharge introduced for frequent flyers, effectively placing an additional ‘rate’ of carbon tax predominately on business travellers. In addition a ‘Green Miles’ scheme could be introduced in the short-term. Such a scheme would mean passengers receive a tax discount for the proportion of the fuel requirement that is sourced sustainably.

- The Climate Change Levy and Climate Change Agreements should be reviewed again in light of the 2050 net zero target to ensure they fully reflect the carbon content of the fuel being used by businesses. The Government should consult on extending carbon pricing further across energy usage in non-residential and public buildings. Many businesses are subject to the Climate Change Levy (CCL) that puts a carbon price on energy usage across a range of fuels. This acts as an incentive to invest in energy efficiency improvements and consider switching to lower-carbon forms of heating. While changes have been made recently to the Climate Change Levy, electricity still attracts a lower rate than gas use, something that will become untenable once coal is completely removed from the power system in 2024. The Government should therefore review the CCL again in light of the likely trajectory to the 2050 net zero target, making further changes to ensure the carbon prices the scheme delivers are sufficient.

- A consistent ‘Climate Change Charge’ should be introduced for domestic energy use linked to underlying UK ETS prices that applies across both electricity and gas use, offset by removing low-carbon levies from bills and providing dedicated support for low-income households. While households already pay the pass-through costs of various carbon pricing schemes – such as the Carbon Price Floor – there is no direct carbon taxation placed on domestic electricity or gas use beyond VAT. This situation is already creating challenges for hitting the 2050 net zero target. The Government should introduce a consistent ‘Climate Change Charge’ across both electricity and gas that reflects the carbon content of both fuels, linked to underlying UK ETS prices.

- Link the new farm payments scheme more directly to the delivery of projects that reduce or store carbon. In addition, before 2030, trial the introduction of tradeable credit markets based on carbon sequestration allowing a long-term route to land-use being included in a dedicated cap-and-trade model. The Government should also establish a ‘Farmland Carbon Code’ to ensure adequate verification of the carbon saved across the agricultural sector. The new Environmental Land Management (ELM) system, influenced in large part by previous Bright Blue policy work[36] has more deeply enshrined the notion of ‘public money for public good’, offering ways for farmers to secure support in relation to taking actions that will support the environment. After the initial pilots, the Government should set a specific target for what the ELM scheme should deliver in terms of carbon savings. This would, in effect, require a specific portion of farm payments to then be spent on carbon-based reduction projects, with requirements rising steadily over time as the target carbon savings required under the scheme grows.

- Reform the Landfill Tax so it is based on a carbon metric. Over the medium-term, include the waste and recycling sector in the UK ETS. The Landfill Tax is already in place but is not linked directly to greenhouse gas emissions. A first step would be to link the landfill tax directly to the carbon content of waste. Given the waste and recycling sector is, in effect, an industrial process, the most obvious next step would be to eventually include the sector within the UK ETS.

Helps to address regional imbalances, thereby levelling up the country

Helps to address regional imbalances, thereby levelling up the country

The current Conservative Government’s flagship policy objective of ‘levelling up’ the country is one that many Governments over the years have attempted. It is a gargantuan task: geographical inequality in the UK is, on some measures, comparable to the economic divide between East and West Germany around 1990.[37] Remedying the UK’s regional imbalances will require a mix of many policies, of which tax is one.

Nevertheless, in some ways the tax system actively holds back progress on levelling up. As house prices have risen relatively faster in some areas, Council Tax falls disproportionately on properties outside of London and the South East: while properties in areas such as Hartlepool might pay in excess of 1% of their value in Council Tax, in areas such as Westminster this can be as low as 0.1%, according to the Institute for Fiscal Studies.[38] While the British tax system is progressive overall, Council Tax is one of the only taxes that is outright regressive.

Stamp Duty Land Tax also plays a part in slowing progress on levelling up. By creating a disincentive for people to move house, the tax slows the housing market. It discourages older residents from downsizing and prevents growing families from moving to bigger houses, promoting inefficient use of living space. Estimates from the LSE suggest that even a two percentage-point increase in SDLT reduces mobility by 37%.[39]

Another central aspect of levelling up is improving equality of opportunity: indeed, the Prime Minister himself said “talent and genius is distributed equally, but opportunity is not”.[40] Inheritances are increasing as a proportion of lifetime income.[41] If left unchecked, this is likely to entrench intragenerational inequalities, with implications for social mobility. Fairly taxing inheritances and gifts will be a helpful tool to reduce the role of geography and affluence at birth in determining life outcomes.

At the moment, though, there are many ways for the richest estates to avoid Inheritance Tax: Business Property Relief and Agricultural Property Relief, which reduce overall liabilities, have loose eligibility criteria. For example, shares on the Alternative Investment Market can attract Business Property Relief, with no requirements for minimum shares in a company and no need to prove a personal relationship to the company.[42] And wealthy estates have the ability to avoid the tax altogether if wealth is passed on well before death thanks to the ‘seven-year rule’. Because of this, the very wealthiest estates pay proportionately less in Inheritance Tax: while most estates were found by the Office of Tax Simplification to pay an effective rate of 20%, for the very wealthiest estates – valued at £10 million or more – the effective rate was 10%.[43]

The tax system can do more to level up institutions as well as individuals. Manufacturing businesses tend to be highly capital-intensive relative to service businesses, and so would stand to gain the most from better capital allowances and incentives to invest through the tax system. They also tend to be based in areas outside of London and the South-East, particularly contributing to jobs and output in the Midlands and the North.[44] Besides being pro-business in general, tax reforms to stimulate investment would aid the levelling up agenda.

Business Rates, too, have a regional bias. As a result of infrequent revaluations that lag behind economic cycles, firms in areas with rising property prices can be caught out by sudden and substantial increases in their Business Rates liabilities. Conversely, businesses in areas with falling property prices can pay over the odds in Business Rates for years until the next revaluation. There is scope to smooth these fluctuations and reduce the compliance costs to businesses.[45]

Some tax policy options for enabling levelling up include:

- Replace Council Tax and Stamp Duty Land Tax with an Annual Proportional Property Tax (APPT) on the capital value of houses. Properly designed, an APPT would be considerably more progressive than the current system of Council Tax and Stamp Duty Land Tax: in most scenarios, lower value properties would pay less in property taxes, while higher value properties would pay more. Moving to an APPT would also be regionally progressive, lowering taxes in areas such as the North West and shifting property taxes to London and the South East.

- Replace Inheritance Tax with a Lifetime Receipts Tax (LRT). The LRT should have a starting lifetime allowance of £125,700. The headline rates should mirror Income Tax rates from now, with the threshold set at ten times the Income Tax salary thresholds. By including lifetime transfers of wealth, and making taxes on inheritances harder to avoid, the LRT would curtail the role of geography and background in determining life outcomes, thus helping to spread opportunity.

- Move to the full immediate expensing of capital investment in new plants, machinery, and industrial buildings when the investment super-deduction expires in 2023. Investment in new plants and machinery would be treated in the same way as any other business expense. Moving to full expensing permanently after 2023 for all capital investment would reduce the marginal effective tax rate for investment to zero, benefitting in particular manufacturing industries in areas outside of London and the South-East.

- Business Rates should be replaced with a Business Land Tax levied on commercial landowners, based on unimproved land values. This would move the Business Rates system away from taxing investments in commercial property, and focus the tax squarely on the economic rent flowing from the value of unimproved land. This would, in particular, benefit manufacturing businesses who often need to invest in industrial equipment such as blast furnaces.

Acknowledgements

This report, and the tax reform project generally, has been made possible by the generous support of Social Enterprise UK and the Joffe Trust. The ideas expressed in this publication do not necessarily reflect the views of our sponsors.

We would like to thank Alex Jacobs from the Joffe Trust and Andrew O’Brien from Social Enterprise UK for their support, patience and advice throughout the project.

Endnotes

[1] ONS, “Consumer price inflation, UK: March 2022”, https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/march2022 (2022).

[2] OBR, “Economic and fiscal outlook – March 2022”, https://obr.uk/efo/economic-and-fiscal-outlook-march-2022/ (2022).

[3] Philip Brien and Matthew Keep, “Public spending during the Covid-19 pandemic”, https://researchbriefings.files.parliament.uk/documents/CBP-9309/CBP-9309.pdf (2022).

[4] GOV.UK, “Spring statement tax plan”, https://www.gov.uk/government/publications/spring-statement-2022-documents/spring-statement-tax-plan (2022).

[5] Steven Pinker, Enlightenment now: The case for Reason, Science, Humanism and Progress (London, 2018), 110.

[6] John Curtice, “Have voters embraced a bigger state?”, https://onlinelibrary.wiley.com/doi/full/10.1111/newe.12264 (2021).

[7] GOV.UK, “Spring statement tax plan”.

[8] ONS, “GDP monthly estimate, UK : February 2022”, https://www.ons.gov.uk/economy/grossdomesticproductgdp/bulletins/gdpmonthlyestimateuk/february2022 (2022).

[9] ONS, “Unemployment rate (aged 16 and over, seasonally adjusted): %”, https://www.ons.gov.uk/employmentandlabourmarket/peoplenotinwork/unemployment/timeseries/mgsx/lms (2022).

[10] OBR, “Economic and fiscal outlook”.

[11] ONS, “Consumer price inflation”.

[12] GOV.UK, “Chancellor announces tax cuts to support families with cost of living”, https://www.gov.uk/government/news/chancellor-announces-tax-cuts-to-support-families-with-cost-of-living (2022).

[13] Sam Dumitriu, “Energising enterprise”, http://www.brightblue.org.uk/wp-content/uploads/2022/03/Energising-enterprise.pdf (2022).

[14] Pascale Bourquin, Robert Joyce and David Sturrock, “Inheritances and inequality over the life cycle: what will they mean for younger generations?”, https://ifs.org.uk/publications/15407 (2021).

[15] Josh Buckland, “Green money: a plan to reform UK carbon pricing”, http://www.brightblue.org.uk/wp-content/uploads/2021/07/Green-money.pdf (2021).

[16] Arun Advani and Andy Summers, “How much tax do the rich really pay? New evidence from tax microdata in the UK”, https://warwick.ac.uk/fac/soc/economics/research/centres/cage/manage/publications/bn27.2020.pdf (2021).

[17] Dumitriu, “Energising enterprise”.

[18] GOV.UK, “Super-deduction”, https://www.gov.uk/guidance/super-deduction (2021).

[19] Dumitriu, “Energising enterprise”.

[20] Ibid.

[21] Ibid.

[22] ONS, “UK government debt and deficit: September 2021”, https://www.ons.gov.uk/economy/governmentpublicsectorandtaxes/publicspending/bulletins/ukgovernmentdebtanddeficitforeurostatmaast/september2021 (2021).

[23] OBR, “Fiscal risks report – July 2021”, https://obr.uk/docs/dlm_uploads/Fiscal_risks_report_July_2021.pdf#page=15 (2021).

[24] House of Commons Library, “National Insurance Contributions Bill”, https://researchbriefings.files.parliament.uk/documents/RP13-60/RP13-60.pdf (2013).

[25] Resolution Foundation, “Chancellor prioritises his tax cutting credentials over low-and-middle income households with £2 in every £3 of new support going to the top half”, https://www.resolutionfoundation.org/press-releases/chancellor-prioritises-his-tax-cutting-credentials-over-low-and-middle-income-households-with-2-in-every-3-of-new-support-going-to-the-top-half/ (2022).

[26] IFS, “Spring Statement 2022”, https://ifs.org.uk/spring-statement-2022 (2022).

[27] Stuart Adam, Louis Hodge, David Phillips and Xiaowei Xu, “Revaluation and reform: bringing council

tax in England into the 21st century”, https://ifs.org.uk/uploads/R169-Revaluation-and-reform-bringing-council-tax-in-England-into-the-21st-century.pdf (2020).

[28] GOV.UK, “Council tax rebate: factsheet”, https://www.gov.uk/guidance/council-tax-rebate-factsheet (2022).

[29] Jonah Fisher, “Climate change: Can the UK afford its net zero policies?”, BBC News, 23 February, 2022.

[30] Buckland, “Green money”.

[31] Michael Johnson, “Tackling intergenerational inequity at its roots”, https://www.brightblue.org.uk/tackling-intergenerational-inequity-at-its-roots/ (2019).

[32] Adam Corlett, Andrew Dixon, Dominic Humphrey & Max von Thun, “Replacing business rates: taxing land, not investment”, https://d3n8a8pro7vhmx.cloudfront.net/libdems/pages/43666/attachments/original/1535625230/embedpdf_Autumn18_Business_Rates.pdf?1535625230 (2018).

[33] IPCC, “Summary for Policymakers of IPCC Special Report on Global Warming of 1.5°C approved by governments”, https://www.ipcc.ch/2018/10/08/summary-for-policymakers-of-ipcc-special-report-on-global-warming-of-1-5c-approved-by-governments/ (2018).

[34] Joshua Burke, Rebecca Byrnes and Sam Fankhauser, “How to price carbon to reach net-zero emissions in the UK”, https://www.lse.ac.uk/GranthamInstitute/wp-content/uploads/2019/05/GRI_POLICY-REPORT_How-to-price-carbon-to-reach-net-zero-emissions-in-the-UK.pdf (2019).

[35] Buckland, “Green money”.

[36] Ben Caldecott, Sam Hall & Eamonn Ives, “A greener, more pleasant land: a new market-based commissioning scheme for rural payments”, http://www.brightblue.org.uk/portfolio/a-greener-more-pleasant-land-a-new-market-based-commissioning-scheme-for-rural-payments/ (2017).

[37] David Behrens, “Britain’s regions less equal than divided Germany, UK2070 conference hears”, Yorkshire Post, 13 June, 2019.

[38] Adam et al., “Revaluation and reform”.

[39] Christian Hilber and Teemu Lyytikäinen, “Transfer taxes and household mobility: Distortion on the housing or labor market?”, Journal of Urban Economics (2017), 57-73.

[40] Boris Johnson, tweet on levelling up, https://twitter.com/borisjohnson/status/1198340442451935232?lang=en-GB (2019).

[41] Pascale Bourquin, Robert Joyce and David Sturrock, “Inheritances and inequality over the life cycle: what will they mean for younger generations?”, https://ifs.org.uk/publications/15407 (2021).

[42] Sam Robinson and Ryan Shorthouse, “Rightfully rewarded: reforming taxes on work and wealth”, http://www.brightblue.org.uk/wp-content/uploads/2022/01/Rightfully-Rewarded.pdf (2022).

[43] OTS, “Office of Tax Simplification: Inheritance Tax Review”, https://www.gov.uk/government/publications/office-of-tax-simplification-inheritance-tax-review (2018).

[44] Make UK, “Regional manufacturing outlook 2019”, https://www.makeuk.org/-/media/eef/files/reports/industry-reports/make-uk-bdo-regional-manufacturing-outlook-2019.pdf (2019).

[45] CBI, “Business rates system is entrenching regional inequalities – CBI President”, https://www.cbi.org.uk/media-centre/articles/business-rates-system-is-entrenching-regional-inequalities-cbi-president/ (2019).

[Image: Pixabay]

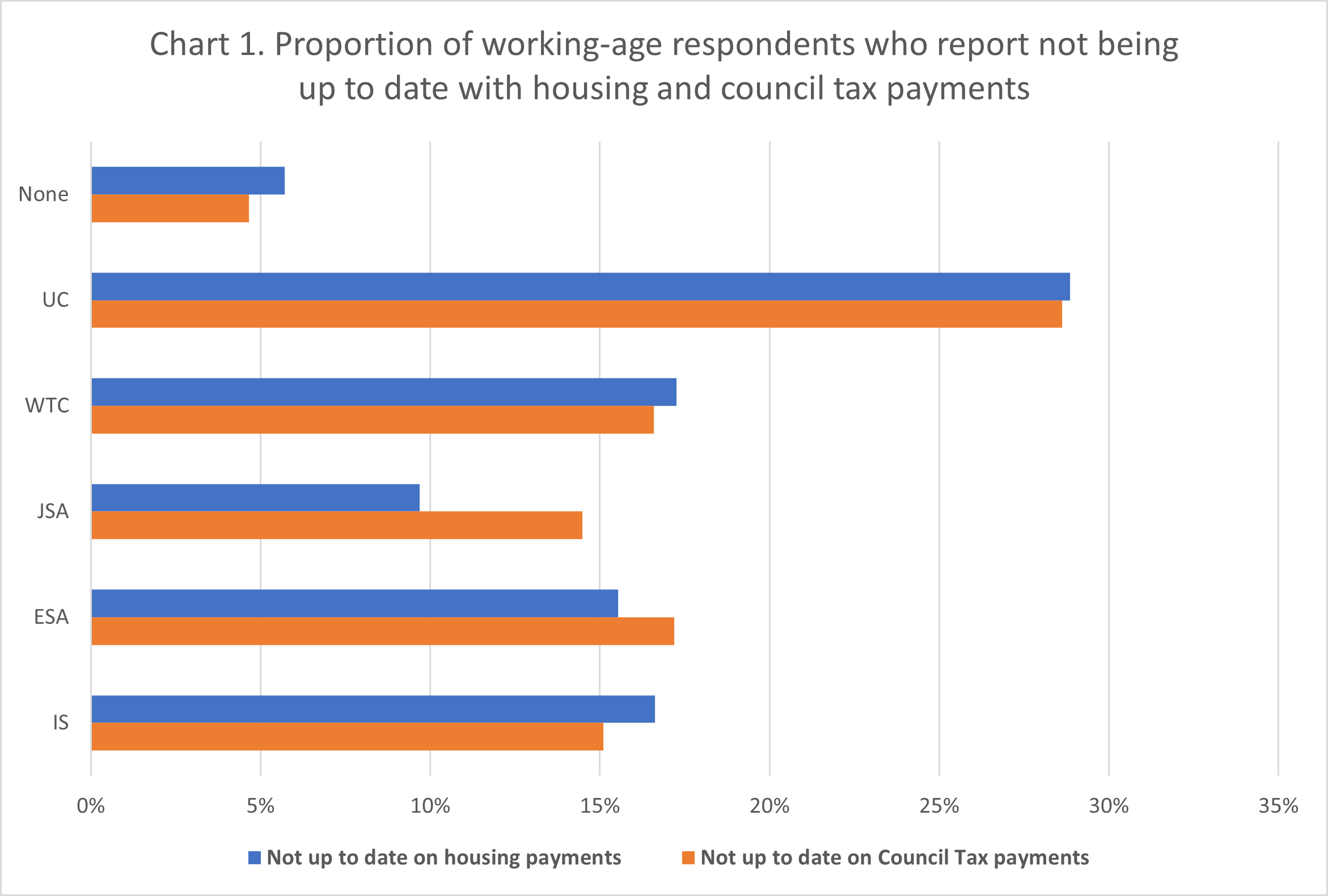

Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021).

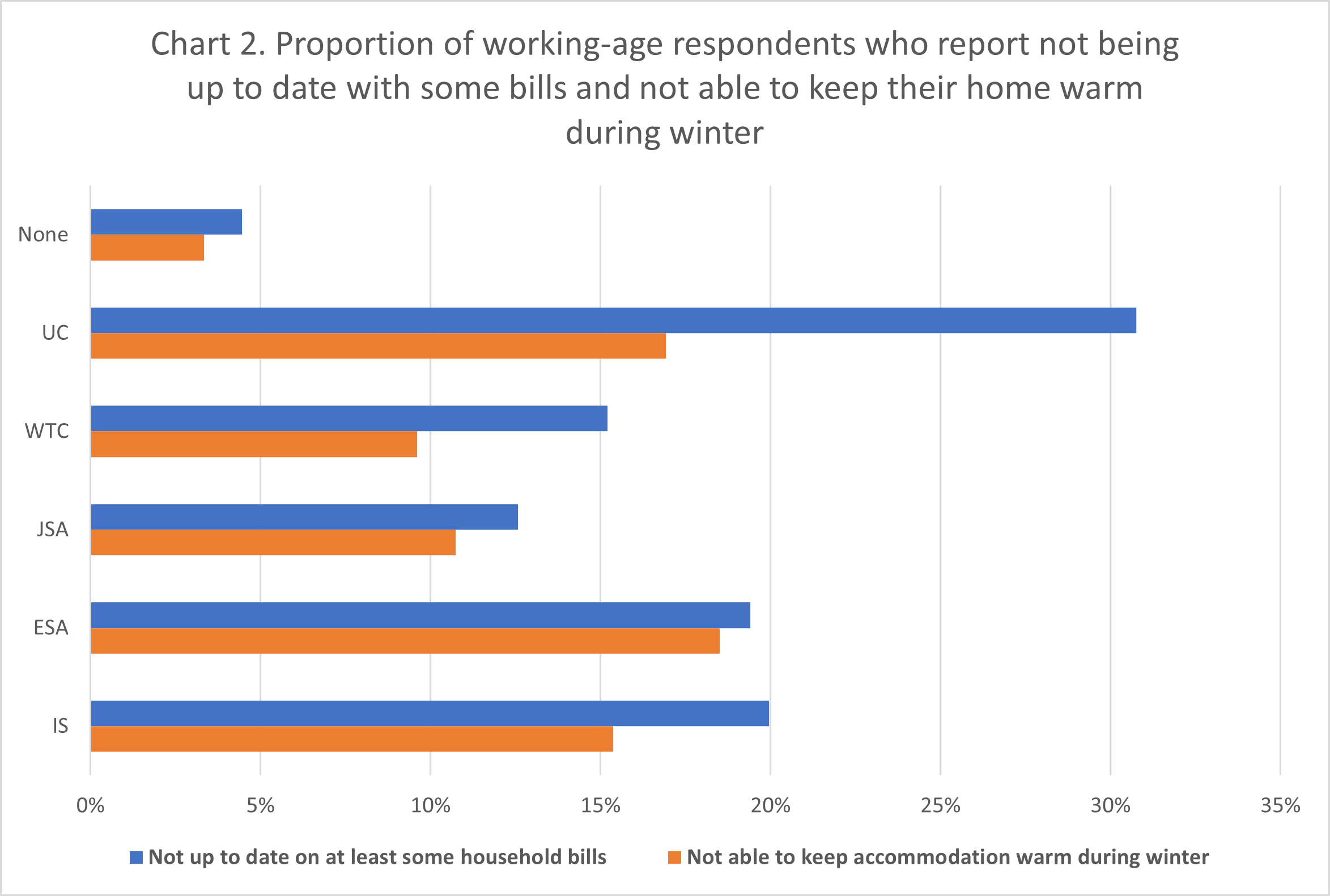

Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021). Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021).

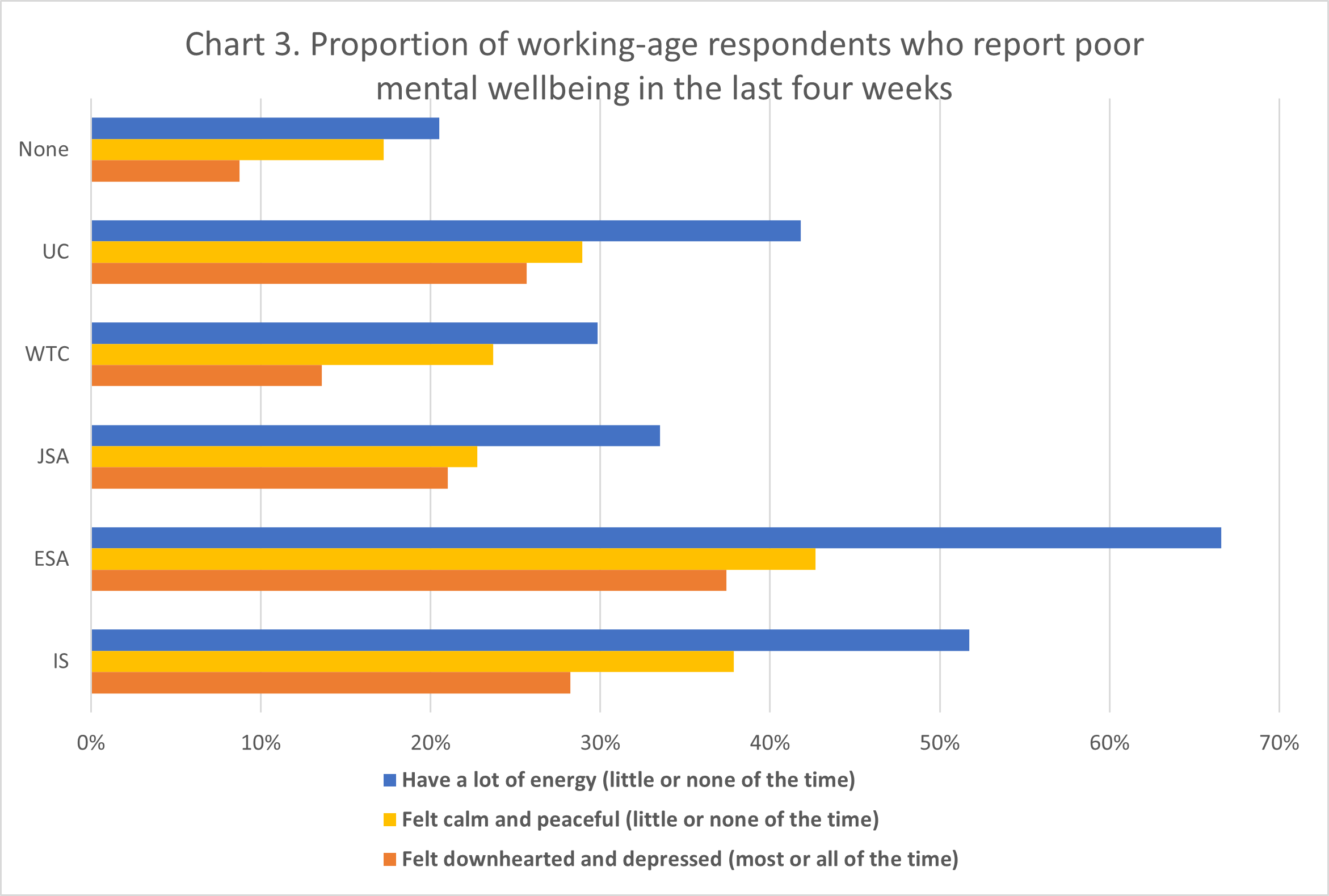

Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021). Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021).

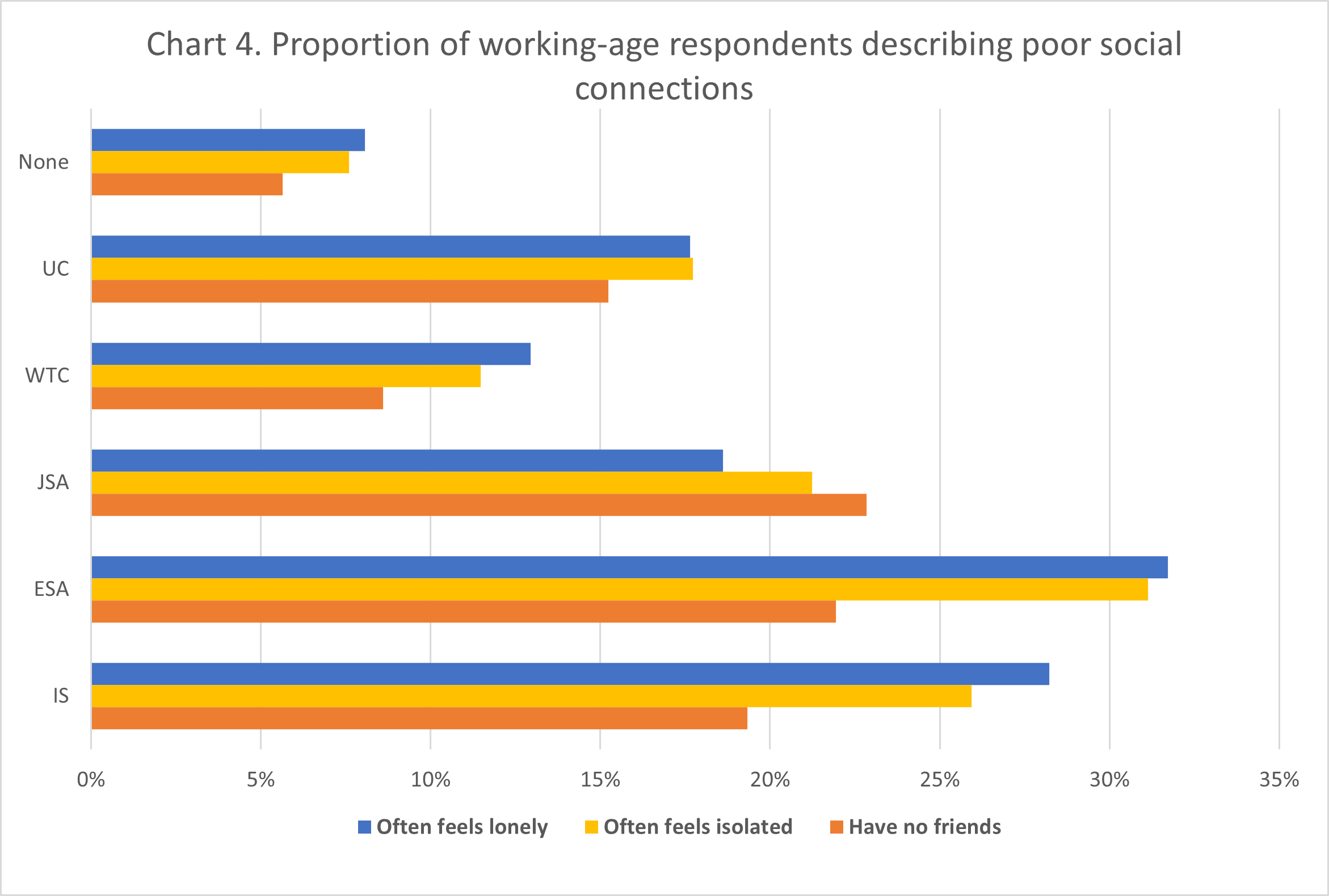

Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021). Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021).

Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021). Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021).

Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021). Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021).

Source: University of Essex, Institute for Social and Economic Research, NatCen Social Research, Kantar Public. Understanding Society: Wave 11, 2019-2021, (2021).

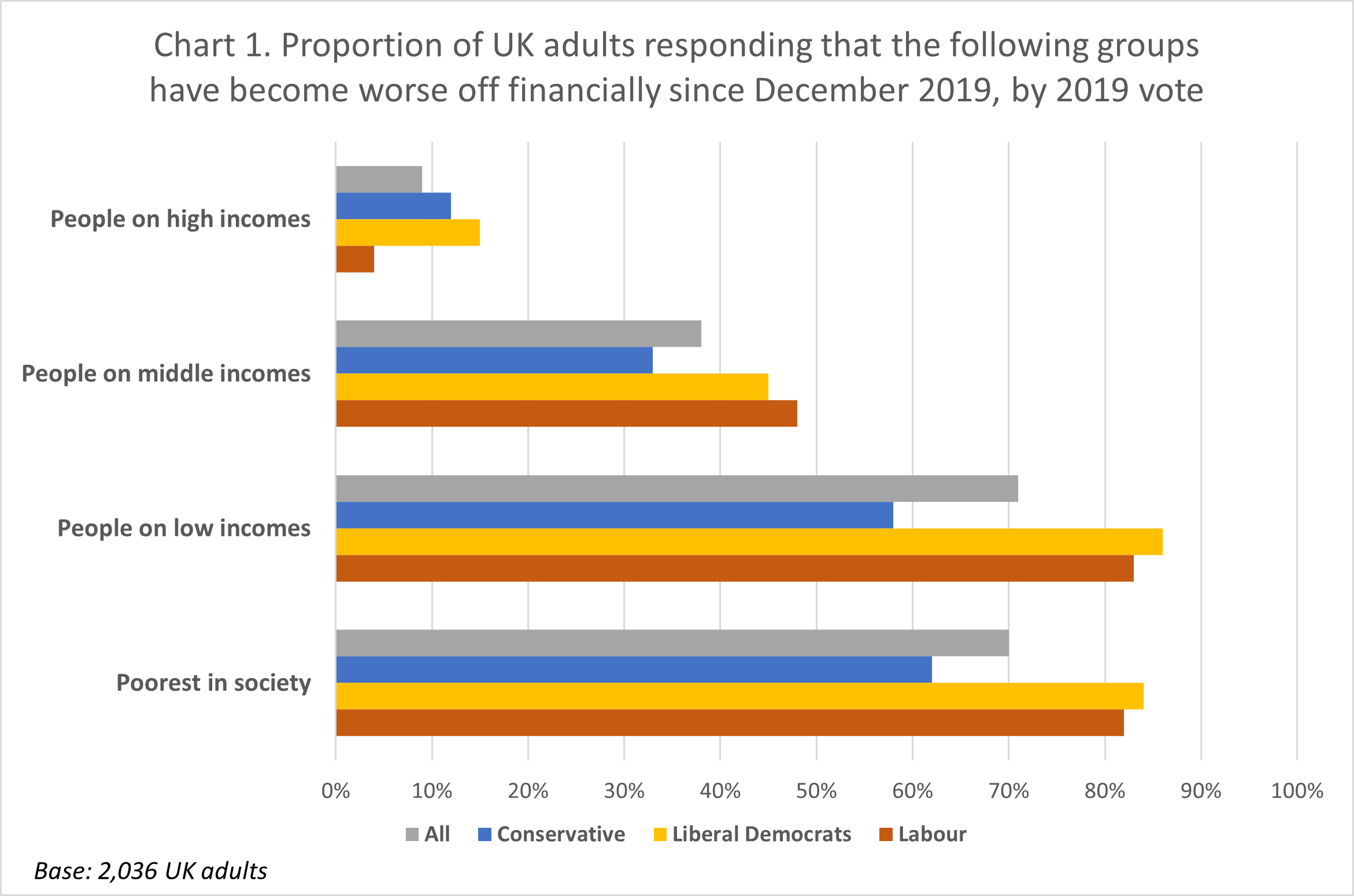

The UK public clearly thinks that more affluent income groups have been less likely to suffer financially since the last general election, with very few people (9%) thinking that those on high incomes have become financially worse off since December 2019, a significant minority (38%) thinking that people on middle incomes have become financially worse off, and large majorities thinking that those on low incomes (71%) and the poorest (70%) have become financially worse off since December 2019.

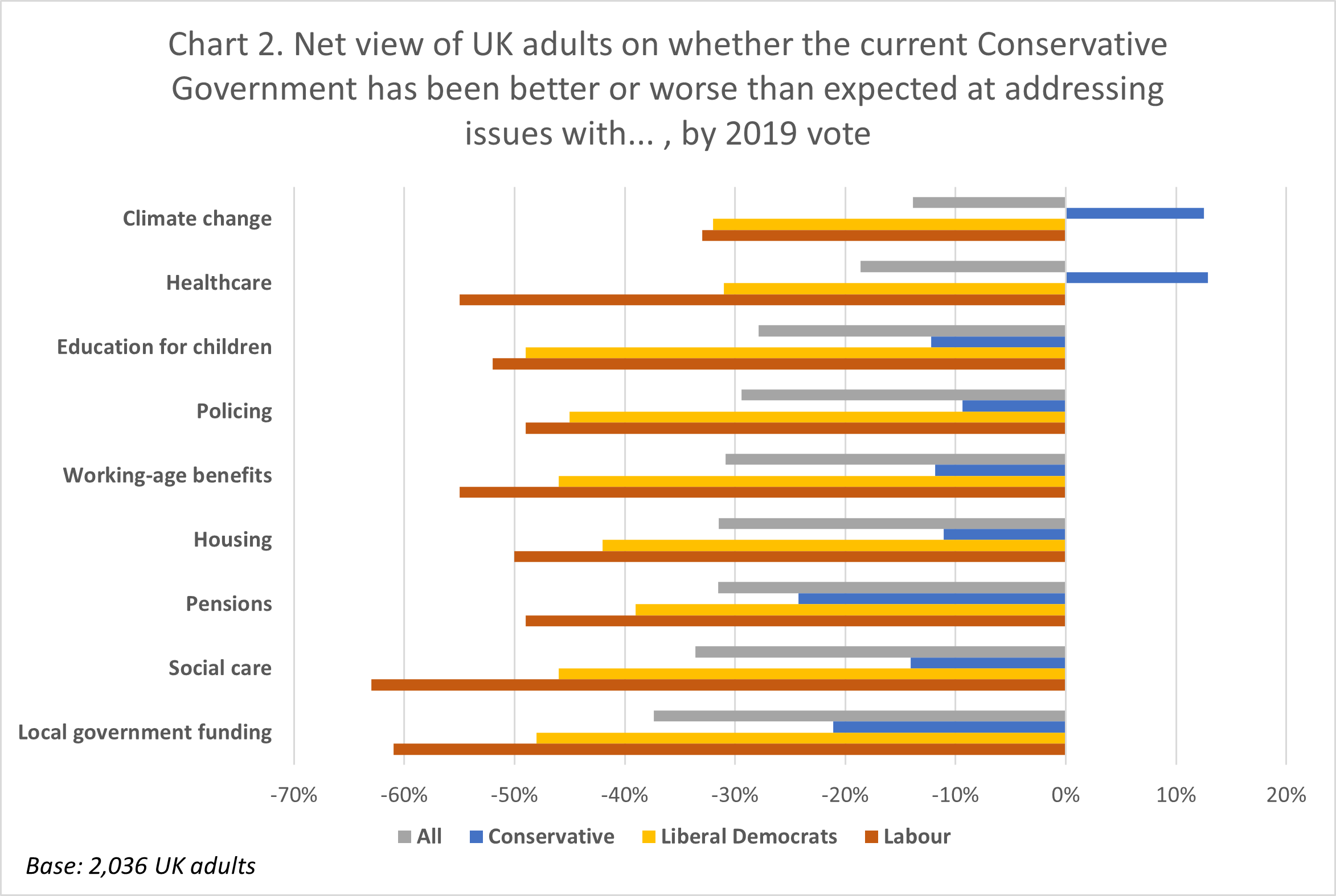

The UK public clearly thinks that more affluent income groups have been less likely to suffer financially since the last general election, with very few people (9%) thinking that those on high incomes have become financially worse off since December 2019, a significant minority (38%) thinking that people on middle incomes have become financially worse off, and large majorities thinking that those on low incomes (71%) and the poorest (70%) have become financially worse off since December 2019. The UK public is more likely to say that the Government has been worse, rather than better, than expected on all the key policy issues polled. Notably, climate change (-14%) and healthcare (-19%) receive the highest net score, while local government funding (-37%) and social care (-34%) receive the lowest net scores.

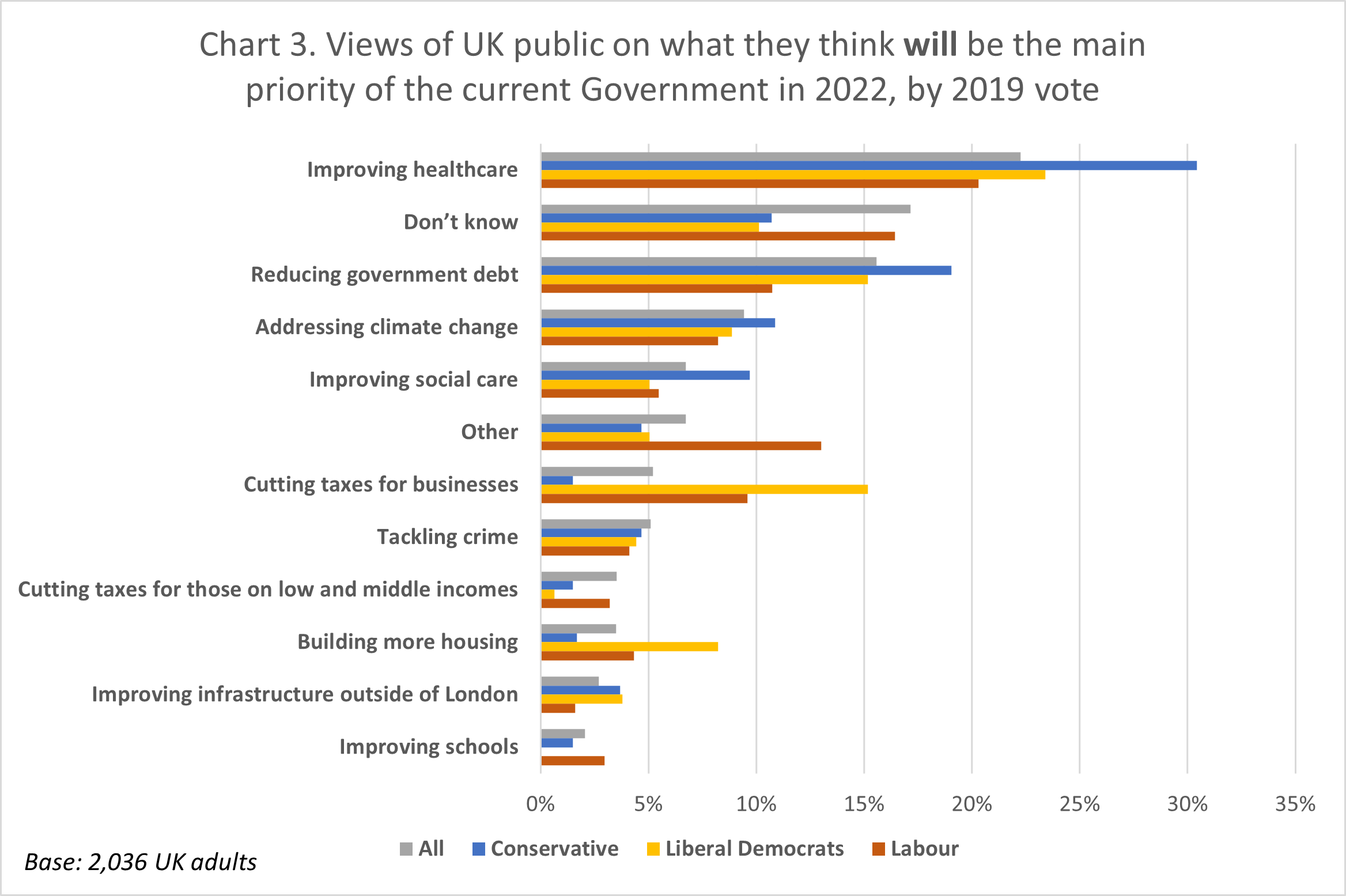

The UK public is more likely to say that the Government has been worse, rather than better, than expected on all the key policy issues polled. Notably, climate change (-14%) and healthcare (-19%) receive the highest net score, while local government funding (-37%) and social care (-34%) receive the lowest net scores.  Improving healthcare is seen as the most likely main priority of the current Government in 2022, with 22% of the UK public thinking that this will be the main priority. This is more likely to be said by 2019 Conservative voters (30%) than 2019 Labour voters (20%).

Improving healthcare is seen as the most likely main priority of the current Government in 2022, with 22% of the UK public thinking that this will be the main priority. This is more likely to be said by 2019 Conservative voters (30%) than 2019 Labour voters (20%).

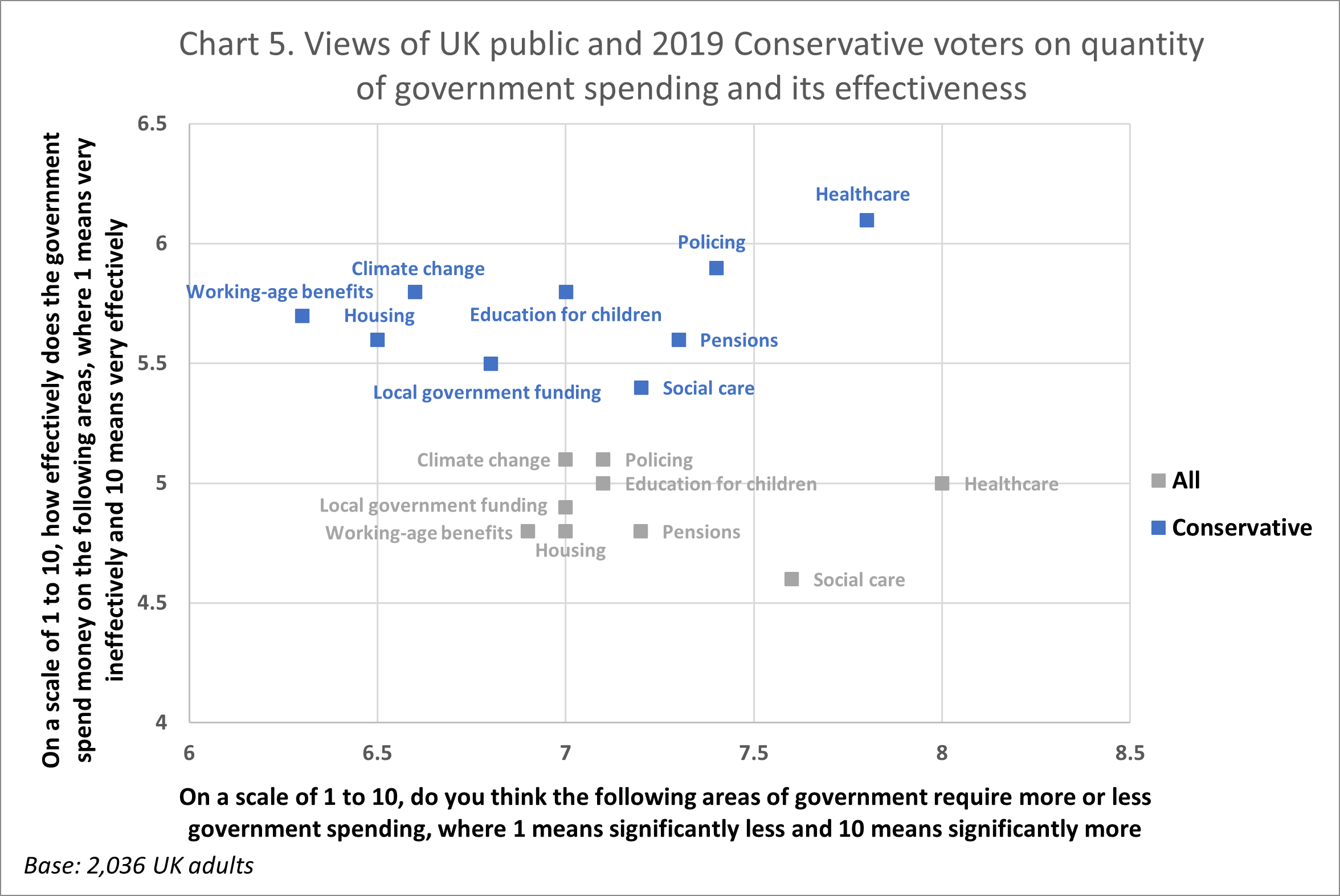

It is notable that the public as a whole, and 2019 Conservative voters, want to see more spending on average, with healthcare receiving the highest average score (8.0 and 7.8 out of 10 on average respectively), while working-age benefits received the lowest average score (6.9 and 6.3 on average respectively), but which is still indicative of greater support for more spending. While 2019 Conservative voters are slightly less likely than the public to be supportive of more spending on key government policy areas, they would still like to see more for all policy areas polled.

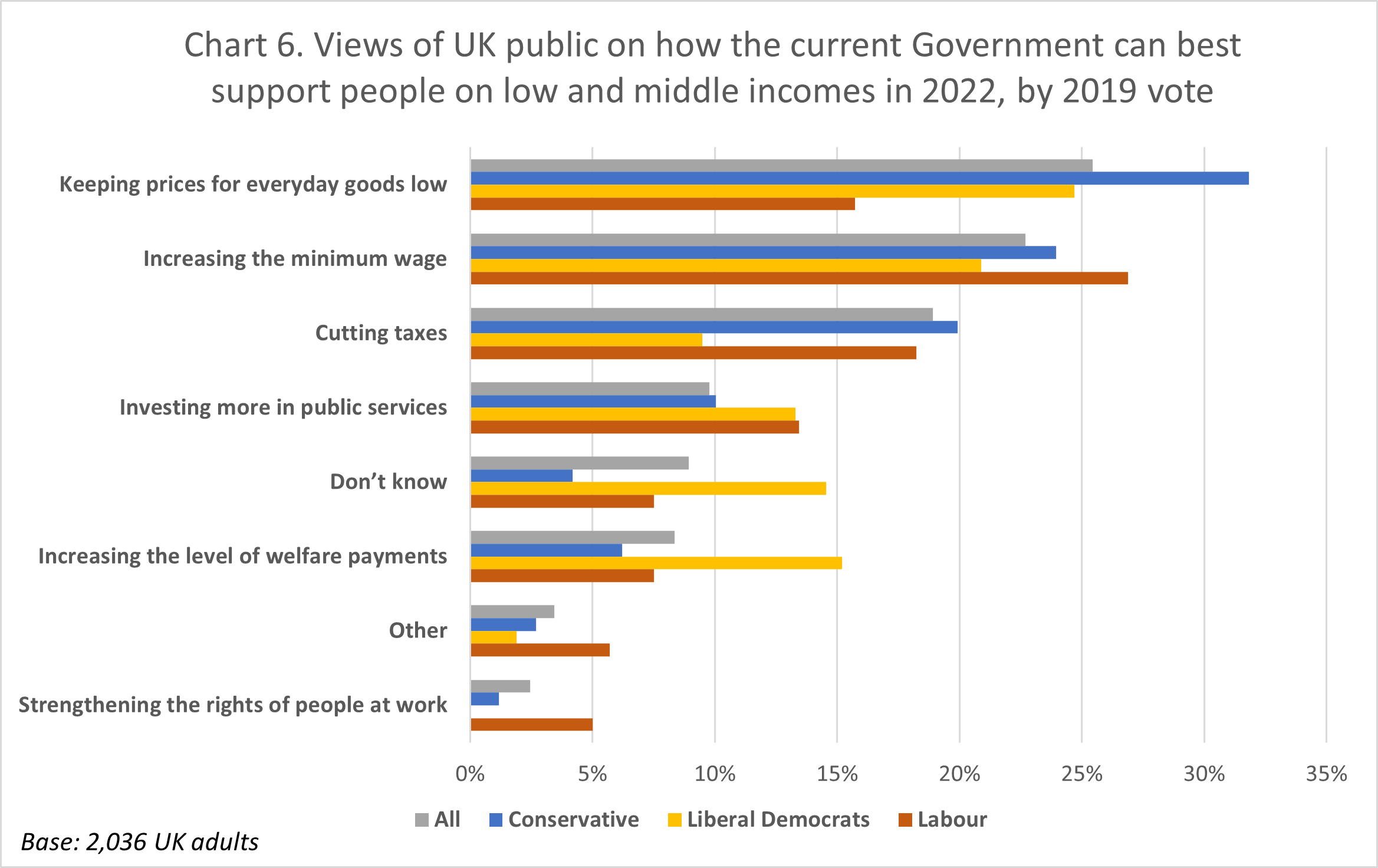

It is notable that the public as a whole, and 2019 Conservative voters, want to see more spending on average, with healthcare receiving the highest average score (8.0 and 7.8 out of 10 on average respectively), while working-age benefits received the lowest average score (6.9 and 6.3 on average respectively), but which is still indicative of greater support for more spending. While 2019 Conservative voters are slightly less likely than the public to be supportive of more spending on key government policy areas, they would still like to see more for all policy areas polled.  Keeping prices for everyday goods low (25%), increasing the minimum wage (23%) and cutting taxes (19%) are seen as the three best ways to help people on low and middle incomes by the UK public. The same ranking is given by 2019 Conservative voters, with keeping prices for everyday goods low (32%) coming first, followed by increasing the minimum wage (23%) and cutting taxes (19%). However, 2019 Labour voters are most likely to prioritise increasing the minimum wage (27%), followed by cutting taxes (18%) and keeping prices for everyday goods low (16%).

Keeping prices for everyday goods low (25%), increasing the minimum wage (23%) and cutting taxes (19%) are seen as the three best ways to help people on low and middle incomes by the UK public. The same ranking is given by 2019 Conservative voters, with keeping prices for everyday goods low (32%) coming first, followed by increasing the minimum wage (23%) and cutting taxes (19%). However, 2019 Labour voters are most likely to prioritise increasing the minimum wage (27%), followed by cutting taxes (18%) and keeping prices for everyday goods low (16%).  Among the UK public, providing grants and loans to businesses affected by the pandemic (28%), cutting taxes (18%) and providing more apprenticeships and training schemes (15%) are seen as the best three ways to support businesses in 2022. Both 2019 Conservative voters and 2019 Labour voters see providing grants and loans to businesses affected by the pandemic (33% and 25% respectively) as the best way to support businesses. However, while 2019 Conservative voters selected cutting taxes (20%) and providing more apprenticeships (18%) as the next best ways to support business, 2019 Labour voters selected providing more apprenticeships and training schemes (16%) and keeping prices for everyday goods low (15%).

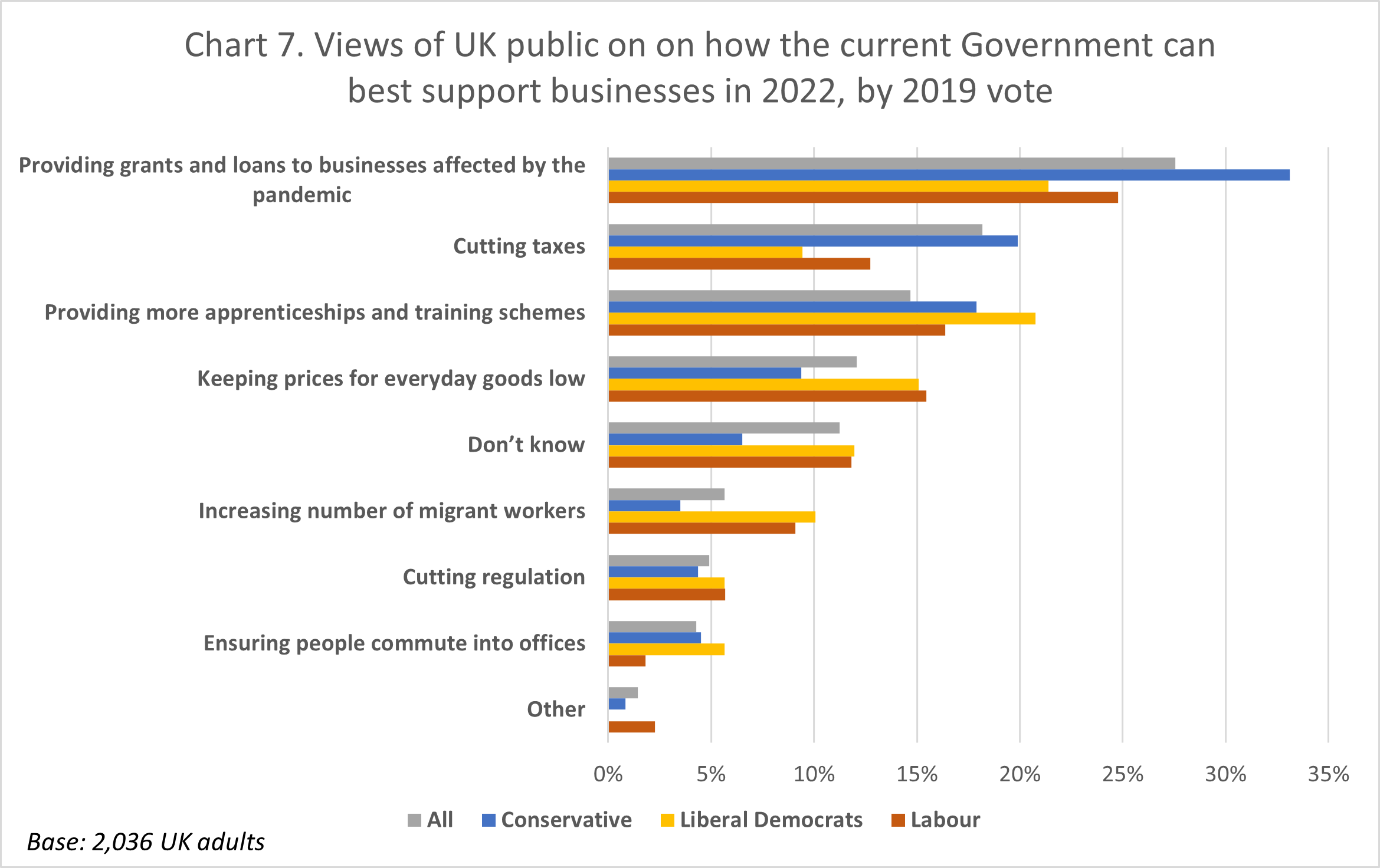

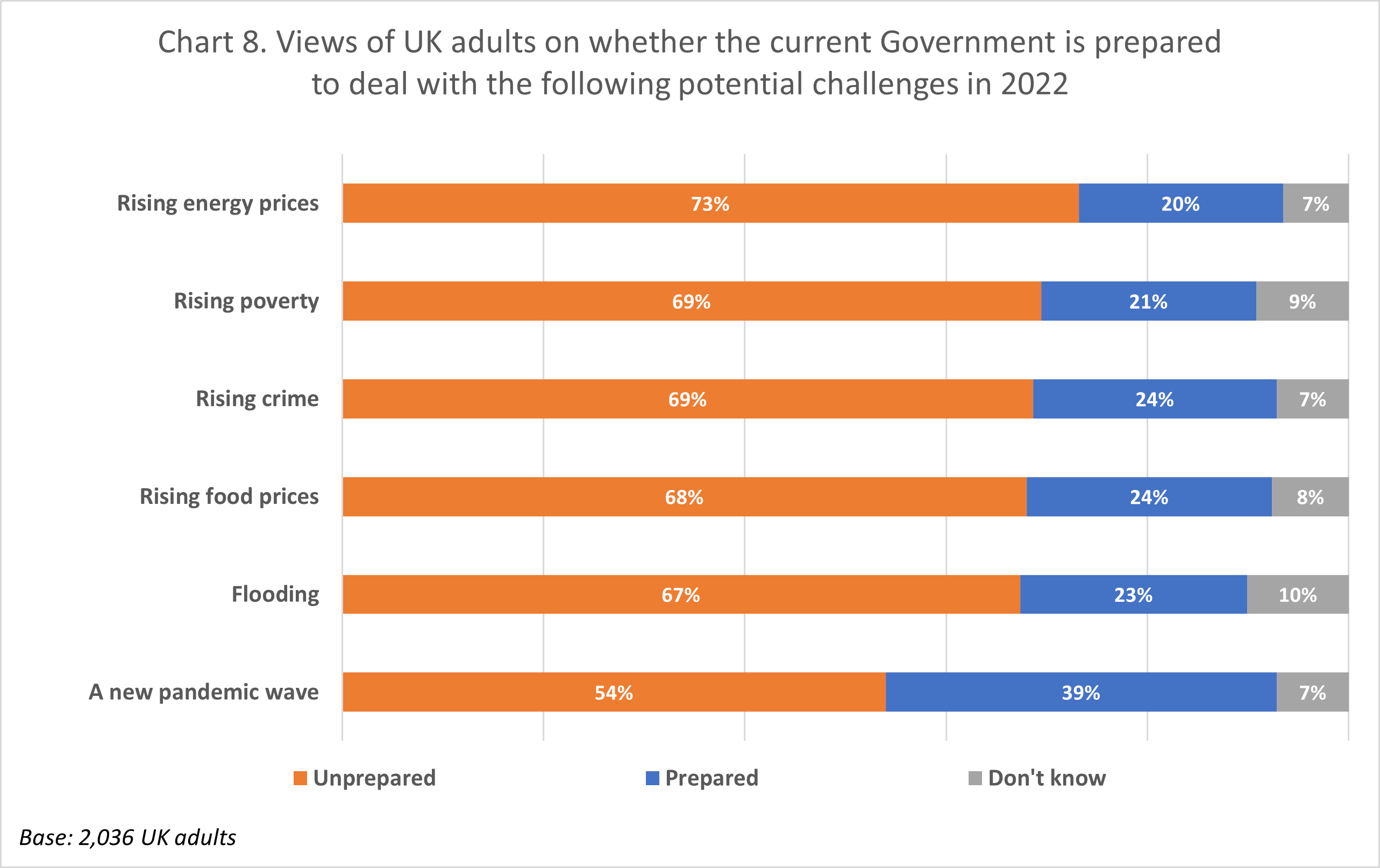

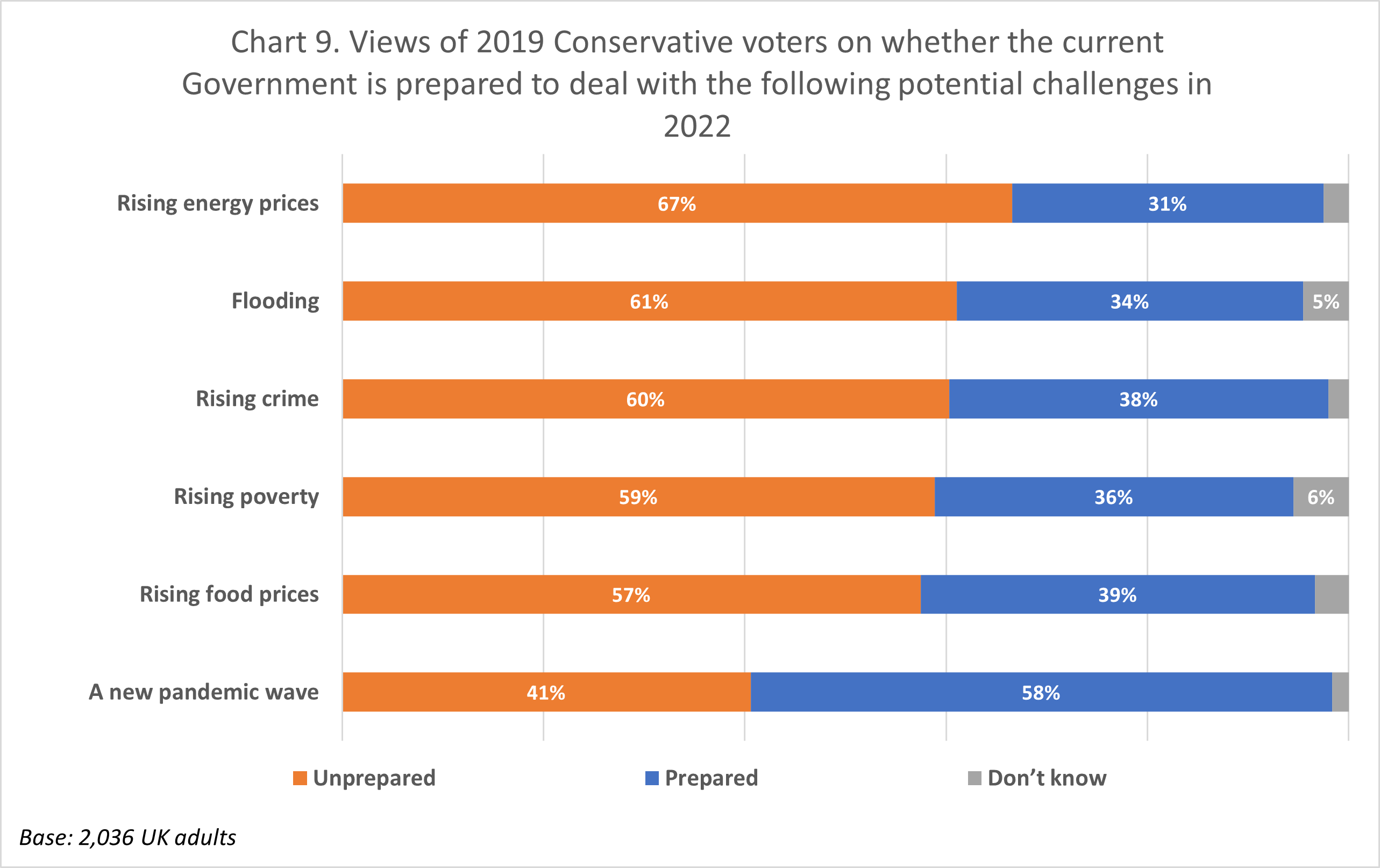

Among the UK public, providing grants and loans to businesses affected by the pandemic (28%), cutting taxes (18%) and providing more apprenticeships and training schemes (15%) are seen as the best three ways to support businesses in 2022. Both 2019 Conservative voters and 2019 Labour voters see providing grants and loans to businesses affected by the pandemic (33% and 25% respectively) as the best way to support businesses. However, while 2019 Conservative voters selected cutting taxes (20%) and providing more apprenticeships (18%) as the next best ways to support business, 2019 Labour voters selected providing more apprenticeships and training schemes (16%) and keeping prices for everyday goods low (15%). As illustrated in Chart 8, the majority of the UK public thinks the current Government is unprepared to deal with all of the polled potential major challenges, with 73% believing that they are unprepared to deal with rising energy prices, 69% believing that they are unprepared to deal with rising poverty, and 69% believing that they are unprepared to deal with rising crime. Even in terms of a new pandemic wave, only 39% believe that the current Government is prepared, while a majority of 54% believe they are unprepared.